Sydney Law Review

|

|

Home

| Databases

| WorldLII

| Search

| Feedback

Sydney Law Review |

|

Evaluating Creeping Acquisitions

Raymond da Silva Rosa,[∗] Michael Kingsbury[†] and

David Yermack[‡]

Abstract

An investor holding over 20% of a public company’s shares can avoid the requirement to mount a takeover bid by accumulating a further 3% every six months, perhaps eventually acquiring control. It has been alleged the practice conflicts with the aim of the Corporations Act 2001 (Cth) that acquisition of control takes place in an efficient, competitive and informed market. We reviewed creeping acquisitions over the ten-year period April 2003 to April 2013 and found no pressing reason for the regulation of creeping acquisitions to be modified on either equity or efficiency grounds. Creeping acquisitions improve the liquidity of shares.

Creeping acquisitions are controversial. It is claimed they ‘may potentially allow an acquirer to avoid paying a takeover premium, ... [and] shareholders in the target company may not have an equal opportunity to participate in the transaction’.[1] Creeping acquisitions were introduced in the Companies (Acquisition of Shares) Act 1980 (Cth),[2] which allowed an investor with at least a 19% shareholding in a company to acquire an additional 3% in each six-month period without making a takeover bid. In a parliamentary debate, it was said the provision is fair because ‘it gives the investors of the target company and also the public at large an indication of what will happen’.[3]

The proposition that creeping acquisitions are transparent has never been tested, perhaps because creeping acquisitions are not salient, the requisite data hard to collect and outcomes difficult to identify. These factors also contribute to an assumption that creeping acquisition activity is trivially small. In 2012, financial reporter Michael Smith observed ‘while the so-called “creep” provision has a sinister ring to it, the rule has rarely been used in Australia to gain control of a company leaving the market divided over whether the rule needs changing or not’.[4]

We reviewed over 50 000 notices of changes in substantial shareholdings lodged with the Australian Securities Exchange (ASX) over the 10-year period 1 April 2003 to 1 April 2013 to assess the frequency and economic significance of equity purchases regulated by the ‘creep provisions’ of the Corporations Act 2001 (Cth) (‘Corporations Act’). Reviewing the notices of changes in substantial shareholding allows us to identify creeping acquisition activity because substantial shareholders hold at least 5% voting power in a company and must lodge a notice every time their voting power changes by 1% or more.

We found that:

(1) Creeping acquisitions are frequent and economically significant, their incidence over the sample period being almost 40% of the number of formal takeover bids and schemes of arrangement that resulted in a change of control.

(2) A substitution effect is evident; the incidence of creeping acquisitions tends to be higher when that of schemes and takeovers is lower.

(3) Most creeping acquisitions occur on-market, but a substantial fraction occur off-market.

(4) The median additional voting power obtained from a creeping campaign is 3%, with about 1.5% obtained every six months.

(5) It is common for creeping acquisitions to be either initiated by investors with close ties to the target board or for them to generate close ties with the board. About 65% of acquirers had a board seat before they started creeping and a further 14% obtained a board seat on their target either during or after their creeping acquisitions.

The above findings and others we report provide an empirical basis to evaluate the validity of several contested claims about creeping acquisitions and the likely effect of proposed regulatory changes. What follows is a brief overview of the economic and legal issues around creeping acquisitions, a description of our research method and then a review and discussion of our findings.

In Australia, an acquirer cannot obtain more than 20% of the voting power in a company without passing through one of the ‘gateways’ in s 611 of the Corporations Act.[5] Takeovers and schemes of arrangement are two common gateways, but their use can be costly. A takeover or scheme entails extensive disclosure, and each requires an acquirer to make equal offers to target shareholders for all, or a proportion of, their shares.[6] In contrast, a creeping acquisition made under s 611(9) may be relatively cheap because it allows for the purchase of more than 20% of the voting power in a company without the need to make an equal offer to target shareholders and with very little disclosure.[7] However, this flexibility is constrained by the caveat that an acquirer’s voting power in its target must not increase by more than 3% every six months when it crosses the 20% threshold.[8]

The Australian Government is considering abolishing creeping acquisitions because they arguably conflict with s 602 of the Corporations Act, which underpins Australia’s takeover law.[9] Section 602 aims to ensure that acquisition of control of voting shares takes place in an efficient, competitive and informed market. The Act’s guide to this outcome are the so-called ‘Eggleston Principles’, named after Sir Richard Eggleston, chairman of the Committee that recommended them in its 1969 report.[10] The Eggleston Principles require that:

(1) shareholders and directors know the identity of any person who proposes to acquire a substantial interest;

(2) shareholders and directors have a reasonable time to consider the proposal;

(3) shareholders and directors are given enough information to enable them to assess the merits of the proposal; and

(4) all shareholders have a reasonable and equal opportunity to participate in any benefits.

If the Eggleston Principles are not followed, then the Takeovers Panel, a peerreview body that regulates corporate control transactions in widely held Australian entities primarily via resolution of takeover disputes,[11] can rule that an acquisition is ‘unacceptable’ and invalid.[12]

In a formal takeover bid, prospective acquirers are required to comply directly with the Eggleston Principles by disclosing to the target in a bidder’s statement: their identity; the offer terms and conditions; financing arrangements; and their post-acquisition plans for the target.[13] Further, a bidder must make equal offers to target shareholders for all, or a proportion of, their shares.[14]

The Eggleston Principles have been subject to criticism, some of it withering. For instance, Sheehy claims ‘it is difficult to see how the Eggleston Principles are “efficient” in any sense of the word’.[15] Critics have noted the Principles increase the cost of acquisitions and thus reduce the level of takeover activity that, in turn, entrenches relatively inefficient managers.[16] For example, Easterbrook and Fischel use a hypothetical to show how requiring all shareholders to receive the same premium can result in some bids being rejected to the detriment of all stakeholders:

[S]uppose that the owner of a control bloc of shares finds that his perquisites or the other amenities of his position are worth $10. A prospective acquiror of control concludes that, by eliminating these perquisites and other amenities, he could produce a gain of $15. The shareholders in the company benefit if the acquirer pays a premium of $11 to the owner of the controlling bloc, ousts the current managers, and makes the contemplated improvements ... If the owner of the control bloc must share the $11 premium with all of the existing shareholders, however, the deal collapses. The owner will not part with his bloc for less than a $10 premium. A sharing requirement would make the deal unprofitable to him, and the other investors would lose the prospective gain from the installation of better managers.[17]

There’s no gainsaying the above argument. However, the critics who mount it tend to discount that equity market regulations reflect a balance between promoting market confidence and liquidity[18] and maintaining incentives for information search and monitoring. Resolving where the balance should lie is a policy issue beyond the scope of this article. Our focus is the more tractable empirical question about whether the creeping acquisitions operate in a way consistent with the Eggleston Principles.

Since at least 1980, when creeping acquisitions were explicitly permitted in the Companies (Acquisitions of Shares) Act 1980 (Cth), the prevailing view has been that they were aligned with the Eggleston Principles. As noted earlier, the creeping provision was defended in Parliament on the premise that investors had ample opportunity to become informed and react accordingly. Speed or rather slowness in transfer of control was seen as critical, as evident by the requirement that an acquirer hold at least 19% of its target’s voting power for six months before crossing the 20% threshold. This characteristic continues to be regarded as essential to the legitimacy of creeping acquisitions. For instance, the Australian Securities and Investments Commission (‘ASIC’) states in its Regulatory Guide 6 (2013) that it may apply to the Takeovers Panel to seek a ruling of ‘unacceptable circumstances’ if creeping does not entail a gradual and open increase in voting power.[19] For its part, the Takeovers Panel agreed in its ruling in The President’s Club Ltd that the creeping provision ‘permits increases in voting power only through a gradual and open process’.[20]

The efficacy of creeping in facilitating a gradual, transparent change in control with equal treatment of shareholders is disputed. As early as 1980, James Graham, an executive director of merchant bank Hill Samuel Australia, predicted that the creeping provision could be used to acquire effective control of a company relatively quickly without the need to accommodate minority shareholders. He said ‘given that the background to the ... legislation was a concern over the increasing use of market raids as a means of acquiring control, it is odd that the [law] formally accepts ... [creeping] practices’.[21] In the United Kingdom (UK), this argument was accepted in 1998 via the repeal of the provision in the UK’s City Code that allowed for acquisitions of 1% per year above the UK’s 30% takeover threshold.[22] The prompt for repeal was the controversy caused by Emerson Electric using the creep provision to take control of Astec Power Company and allegedly depressing its share price to force minority shareholders into accepting a takeover offer.[23]

The influence of high profile cases in shaping public debate on the merits of allowing creeping acquisitions is also evident in Australia. Billionaire investor James Packer crept up the register of the prominent gaming company Crown Ltd, from 37% in 2009 to a majority shareholding of 50% in 2012. Following Packer’s acquisition, ASIC chairman, Greg Medcraft, publicly aired his concern that investors were ‘aggressively seeking control of businesses without paying a premium for other investors’ shares’.[24]

Mr Medcraft’s reported statement reflects a subtle, though perhaps inadvertent, escalation in the ‘protection’ afforded to target shareholders in changes of control. It is not obvious that the drafters and supporters of the 1980 legislation permitting creeping acquisitions would find an increase of 13% in a substantial shareholder’s stake over a three-year period aggressive. More pertinently, the Eggleston Principles do not require that target shareholders be paid a premium in changes of control, but merely that they all have a reasonable and equal opportunity to participate in any benefits.

One basis for all target shareholders sharing in any takeover premium is the view expressed in 1985 by the Australian Companies and Securities Law Review Committee (‘CSLRC’):

[T]he case for any control premium to be vested proportionately in all shares is based on fundamental notions of fairness and equity: a share is a proportionate interest in the enterprise, and no aggregation of shares ought fairly claim entitlement to value derived from the enterprise greater than the sum of the individual value of each share.[25]

This view dates back to work of Berle in the 1930s. He asserted that ‘any premium received by an individual for a sale of control belongs in equity to all of the shareholders’.[26] However, jurisprudence in the UK and the United States (US) has denied his thesis.[27]

Notwithstanding the above, it is arguable creeping triggers a collective action problem that violates the principle that shareholders have reasonable and equal opportunity to participate in any benefits. Even if the optimal choice for shareholders is to hold onto their shares, they may still sell them to a creeping acquirer out of a fear that others may sell out over time and leave them as a minority.[28] A related concern has been expressed by Treasury:

[I]f the acquirer does not make a formal bid [in a creeping acquisition] ... the market may be uncertain as to the details of the proposed acquisition, such as the stake the acquirer ultimately intends to take and what they intend to do when they have control of the company’s assets. This makes it difficult for the target company board to assess the acquisition and make recommendations to shareholders.[29]

Treasury’s argument assumes the acquirer knows the stake it intends ultimately to acquire and that target firm shareholders have a right to this information. The issue here is the set of rights or expectations that an investor has when they buy a share. To paraphrase Shleifer and Vishny,[30] investors do not buy a ticket that yields them a premium with a probability of one if a takeover offer is made. The price of the equity they buy reflects the weaknesses (and strengths) of internal and external control mechanisms. In effect, they are ‘buying a (fairly priced) lottery ticket over the control related outcomes that determine production and dividends’.[31]

In respect of the ‘collective action problem’, it is pertinent to note that not selling out to a creeping acquirer when there is uncertainty about the acquirer’s intentions might be profitable for minority shareholders. As a creeping acquisition progresses, the market may find it easier to infer the intentions of an acquirer and more accurately value its target’s shares closer to the end of an acquisition when control has almost been acquired. For instance, Zingales’ study of the value of voting rights in US corporations shows that as a company’s level of ownership concentration increases, a corporate control contest becomes more likely.[32] He also shows that as a company’s ownership concentration increases, the price of its voting shares increase.[33] In the case of a creeping acquisition, the likelihood of a control contest will become most apparent after an acquirer has increased its voting power substantially over time.

The view that target shareholders should bear a proportionate risk of capturing the benefits of a takeover bid does not address one remaining issue: do the target shareholders have equal opportunity to assess the likelihood of a change of control and potential to earn a premium over the course of a creeping takeover? It is plausible to argue they do when the acquirer creeps via on-market purchases. It is less credible that all target shareholders have an equal opportunity when creeping acquirers accumulate shares via off-market acquisitions. If the creeping acquirers need to increase their stake in the target by just 3% or less to acquire effective control, it could be that most target shareholders may not even know about a change in control until after it occurs. This is one reason why Stephen Mayne, a prominent shareholder activist and director of the Australian Shareholders Association, proposes that takeover law should be reformed to mandate ‘that all creeping must take place on-market’.[34]

In summary, creeping acquisitions are permitted in Australia on the premise that investors have ample and equal opportunity to become informed. Most calls for the abolition or amendment of the creeping takeover provisions dispute this premise in some way. Resolving the issue is made difficult by the lack of information on fundamental points such as the incidence of creeping acquisitions, the manner in which they are conducted, the kinds of firms involved and the outcomes. These are all issues we address in this article; specifically, we answer the following questions:

(1) What is the incidence of creeping acquisitions?

(2) Do creeping acquirers typically accumulate sufficient voting power to achieve control?

(3) What are the avenues through which creeping acquirers accumulate shares?

(4) Are creeping acquisitions typically a substitute for or precursor to a full-fledged takeover bid?

We make use of the substantial shareholding disclosure regime in s 671B of the Corporations Act to identify creeping acquisitions. Under s 671B, a ‘substantial shareholder’ must lodge a notice with the ASX every time that there is a movement in its and its associates’ voting power in a company by at least 1%.[35] If such a change in voting power occurs, a notice must be lodged within two business days after the change.

A ‘change in substantial shareholding’ notice provides a wealth of information useful in identifying creeping activity. For instance, for a change in voting power that occurs above the 20% takeover threshold, the notice typically details the ‘gateway’ in s 611 Corporations Act that permits the change. Thus, it is possible to identify changes in voting power made feasible by the creeping provision in s 611(9), and discard changes that took place on the basis of a takeover, scheme of arrangement, buy-back, rights issue, underwriting, or other exception in s 611. Where a notice does not explicitly state whether share purchases were made under s 611(9), it is possible to infer this if those purchases were made either ‘on-market’ with no concurrent takeover bid, or ‘off-market’ with no concurrent equity issue by the target firm (cross-referenced using Morning Star’s DatAnalysis service and Connect4’s takeover database). In both of these cases, the purchases must have, by definition, occurred solely under s 611(9).

Given the above, we manually reviewed approximately 50 000 notices lodged between the ten-year period 1 April 2003 and 1 April 2013. If a notice related to an increase in voting power above 20% due to s 611(9) we deemed it a creeping acquisition.

Other information collected included:

(1) The date a creeping acquirer started purchasing shares in its target;

(2) The date an acquirer achieved an increase in its voting power in its target of at least 1% and the percentage increase achieved;[36]

(3) Whether an acquirer increased its voting power via on or off-market acquisitions; and

(4) The consideration an acquirer paid to increase its voting power.

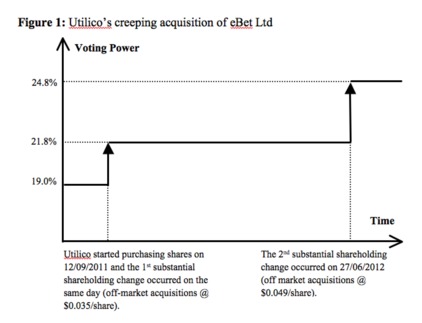

Where an acquirer lodged multiple notices for one target then the information in the notices was combined and counted as one observation. Figure 1 illustrates the process.

Figure 1 shows Utilico’s increases in its holding in eBet Ltd were announced via two notices. One notice disclosed that Utilico increased its voting power by 2.8% through the off-market purchase of 6.47 million shares on 12 September 2011, for $226 333 or $0.035 per share. The other notice disclosed that Utilico increased its voting power by 3.0% through off-market purchases of 6.88 million shares ending on 27 June 2012, for $337 091 or $0.049 per share. We combine the information in the two notices to record that Utilico’s increased its holding in eBet Ltd by 5.8% for $563 424 (ie, a weighted average of $0.042 per share) via an off-market creeping acquisition starting on 12 September 2011 and ending on 27 June 2012.

Note our calculation takes into account the voting power that Utilico acquired between 19% and 20% despite the takeover threshold being 20%. The reason is that s 611(9) requires an acquirer to hold at least 19% of its target’s voting power for six months before crossing the 20% threshold[37] and so we include the purchases that an acquirer makes above 19% if they cross the threshold in the same notice, because all of those purchases are, in effect, governed by the creeping provision.

Two further conditions must be met for an observation to count in our sample. First, the information in a ‘change in substantial shareholding notice’ must be complete. In other words, a notice must detail the voting power that was acquired, the consideration paid per share, and whether the shares were acquired on or offmarket. Second, there must be no confusion about whether the voting power that was acquired was justified by the creeping provision or another exception in s 611 of the Corporations Act.

To ensure we reviewed only those notices that fall under s 611(9), a notice was discarded if any of the information above was unavailable, or there was any confusion. For example, if there was a ‘change in a substantial shareholding’ above 20% that was due to both s 611(9) and another exception under s 611, it was omitted. Similarly, if a notice disclosed that an increase in voting power was due to the exercise of an option or the participation in a placement, it was omitted as that increase in voting power could be justified under s 611(7) — ‘Approval by resolution of target’, or s 611(9).

A ‘change in substantial shareholding’ notice only needs to be lodged under s 671B of the Corporations Act if an acquirer’s voting power changed by at least 1%. Thus, an observation was also omitted if it was for a change that was less than 1%, or consisted of multiple changes for less than 1%. We omit those observations because the acquirers in these cases may be voluntarily signalling their intentions to the market and we wish to focus on those creeping acquisitions most vulnerable to the criticism that target shareholders did not have an equal opportunity to participate in the benefits from a change in control. However, where an acquirer lodged more than one notice and some notices detailed changes in voting power above 1% and some below 1%, that entire observation was not omitted unless the latter notices made up more than one-third of the total number of notices for that creeping acquisition.

Figure 1: Utilico’s creeping acquisition of eBet Ltd

Following the above protocol, we found that 242 creeping acquisitions were ‘in progress’ on the ASX between 1 April 2003 and 1 April 2013. All our findings related to these 242 acquisitions. Twelve of the creeping acquisitions commenced before 1 April 2003 and continued into the sample period. In those cases, we collected information from the start of the ‘program’ of creeping acquisitions.[38] At the other extreme, some creeping acquisitions began during our sample period and would have continued beyond our sample end date.

In our sample, 230 creeping acquisitions began after 1 April 2003. By way of comparison, 607 successful takeovers or schemes were announced over the tenyear period ending 1 April 2013.[39] We concluded that the incidence of creeping acquisitions was not trivially small; over one-fourth of all share purchases above the 20% takeover threshold initiated by an acquirer were done under the auspices of the creeping provision. This figure was an underestimate because we do not include creeping acquisitions where more than onethird of the notices of changes in substantial shareholding announced by the acquirer were for changes less than 1% of voting power.

The number of creeping acquisitions increased over our sample period. The incidence of creeping acquisitions increased by 30% in the second half of the tenyear sample period, during which time the global financial crisis (‘GFC’) occurred. A potential explanation is that market uncertainty following the 2008 financial crisis increased the relative attractiveness of purchasing shares under s 611(9) of the Corporations Act which allows an acquirer to take a cautious, incremental, and arguably cheaper approach to acquiring control, or effective control.

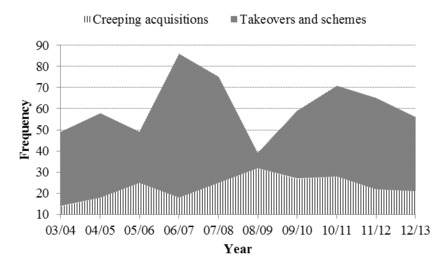

Figure 2, which shows the incidence of creeping acquisitions, takeovers and schemes for each year in the sample, lends support to the above proposition. A modest substitution effect was evident; when takeovers and schemes were relatively popular, creeping acquisitions were relatively less popular. The effect is most noticeable for the years at the height of the GFC, between 2008 and 2009, when the number of creeping acquisitions (32) rose dramatically to almost reach parity with the number of successful takeovers and schemes launched (39) over the same period. Conversely, prior to the GFC, the market ‘bull’ run between 2005 and 2007 saw a rapid increase in traditional mergers and acquisitions (‘M&A’) activity and a decline in creeping acquisitions. Delaying an acquisition of control that generates positive net present value (‘NPV’) is costlier in a bull market.

Figure 2: Incidence of takeovers schemes and creeping acquisitions, 2003–13

The use of creeping acquisitions as a means of mitigating the risk of acquirers while enhancing liquidity in the market for the target firm’s shares over the creep period has not featured in the debate over the merits of s 611(9). While Treasury has accurately stated that creeping acquisitions leave the market uncertain about the stake the acquirer ultimately intends to take and what they intend to do when they have control of the target’s assets, it is reasonable to assume that in many instances the acquirer’s plans may be provisional, particularly in ‘bear’ markets. Our sample data suggest the relative cost of full-fledged takeover bids is higher in a bear market and abolishing creeping acquisition is likely to reduce the market for the shares of potential targets at a time when that liquidity is likely to be most valued.

Table 1 shows the median acquisition of voting power under s 611(9) over our sample period was 3% and the mean was 4.1%, with the standard deviation being 3.32%. The largest acquisition of voting power was 19.80%, which took approximately threeandahalf years to accomplish. If s 611(9) is used to acquire control, it is not, for the most part, through drawn out acquisitions that begin at the 20% level. Instead, s 611(9) is more likely used to acquire ‘effective’ control below 50%, or an ‘absolute’ majority holding if it is used in conjunction with another gateway to further acquisitions in s 611 of the Corporations Act.

Table 1: Voting power and creep intensity (whole sample)

|

|

Voting power acquired (%)

|

|

Creep intensity

(% per six months)

|

|

Time between first and last purchase (months)

|

|

|

|

|

|

|

|

|

Mean

|

4.08

|

1.69

|

15.51

|

||

|

Median

|

3.00

|

1.47

|

6.83

|

||

|

Maximum

|

19.80

|

3.00

|

124.90

|

||

|

Minimum

|

1.00

|

1.00

|

0.00

|

||

|

Std deviation

|

3.32

|

0.86

|

21.83

|

||

Given the Takeovers Panel’s view that creeping acquisitions should be gradual and open, we investigated the speed at which acquirers creep (‘creeping intensity’). Our measure of creeping intensity is the ratio of voting power purchased in a creeping acquisition divided by the number of six-month periods that elapsed during that acquisition (rounded up). Across our sample of 242 acquirers, creeping intensity was typically well below the maximum rate of 3% every six months; the mean and median increases in voting power were 1.69% and 1.47% respectively. The majority of those who used s 611(9) could have purchased more shares over the relevant six-month period than they did.

Perhaps not all acquirers in our sample were intent on acquiring control; their crossing of the 20% threshold may have been happenstance. Given the premise that acquirers that lodged more than one notice of ‘change in substantial shareholding’ (55% of our sample) were more likely to be aiming for influence, we reviewed their acquisitions separately. Indeed, the average voting power acquired by ‘multi-notice’ acquirers is higher than the average across the whole sample. The mean and median increase in the voting power of multi-notice acquirers is 5.87% and 4.90% respectively, almost 2% higher than that for the whole sample. Interestingly, the creeping intensity of multi-notice acquirers is much the same as singlenotice acquirers over our sample period. Multi-notice acquirers used s 611(9) to purchase voting power at a median rate of 1.46% every six months.

Creeping intensity could be low because, pursuant to s 611(9), some acquirers in the sample who started purchasing shares below 20% may have been forced to wait for up to six months to cross the 20% threshold. As those acquirers could not have purchased more than 1% of their target in that six-month period, their intensity rate might be underestimated. We investigated and found that the mean and median acquisition rate for the 167 acquisitions that started at a ‘toehold’[40] on or above 20% was 1.71% and 1.48% every six months. Similarly, the multinotice subset under this criterion had an intensity of 1.64% and 1.46% respectively.

Even the three most experienced creeping acquirers in the sample used s 611(9) well below maximum intensity. The most active acquirer, shown in Table 2, was Guinness Peat Group, a renowned corporate raider.[41] It made eight separate acquisitions using s 611(9). Nevertheless, despite spending over $100 million purchasing shares under the creeping provision, and in the process obtaining two board seats and launching a takeover post-creeping, it did not exploit s 611(9) to the extent that it could have — it only crept at a rate of 1.48% to 1.78% every six months.

It is likely that ‘slow’ creeping reflects ‘gaming’ behaviour: acquisitions at maximum intensity may tip-off other investors causing an increase in target valuations.[42] An acquisition rate below 3% could be cost-efficient, leaving aside the benefits of acquiring control or influence earlier rather than later.

Given that the ability of an acquirer to camouflage its trading is lower in small stocks that are thinly traded, we investigated the association between target firm size and creep intensity. We found that the targets of creeping acquirers are smaller than firms subject to formal takeover bids or schemes designed to pass control. The mean and median market capitalisations of creep targets on the day before an acquirer’s first purchase were $204 million and $35 million respectively. This compares to a mean and median market capitalisation of $717 million and $109 million for targets in takeover bids and schemes during the sample period.[43] As creep targets were mostly small, their presumed low liquidity could be why creeping intensity was also low. However, we found that targets acquired at a rate of more than 2% every six months were smaller than those that were acquired at a rate below 2% — each had median market capitalisations of $33 million and $38 million respectively.

Table 2: Top three creeping acquirers by number of acquisitions

|

|

Guinness Peat Group

|

|

Washington H. Soul Pattinson

|

|

CVC Ltd

|

|

Targets

|

8

|

|

5

|

|

4

|

|

One-off acquisitions

|

2

|

|

2

|

|

1

|

|

Multiple notice acquisitions

|

6

|

|

3

|

|

3

|

|

Target market cap ($ m) (mean)

|

194.31

|

|

368.22

|

|

44.67

|

|

Target market cap ($ m) (median)

|

64.78

|

|

205.03

|

|

47.30

|

|

Consideration ($ m) (mean)

|

12.52

|

|

7.11

|

|

1.78

|

|

Consideration ($ m) (median)

|

8.75

|

|

3.51

|

|

1.40

|

|

Total consideration ($ m)

|

100.19

|

|

58.85

|

|

7.13

|

|

Voting power acquired (mean)

|

5.91

|

|

3.06

|

|

4.99

|

|

Voting power acquired (median)

|

5.91

|

|

2.91

|

|

5.24

|

|

Voting power acquired (max)

|

14.85

|

|

4.89

|

|

6.37

|

|

Creep intensity (%) (mean)

|

1.78

|

|

1.32

|

|

1.74

|

|

Creep intensity (%) (median)

|

1.48

|

|

1.11

|

|

1.68

|

|

Number of acquisitions that

achieved a board seat

|

2

|

|

1

|

|

0

|

|

Takeovers launched within

one year of last notice

|

1

|

|

0

|

|

0

|

Not all of the creeping acquisitions involved small targets. The standard deviation of the targets’ market capitalisations is high — $589 million. In fact, approximately 30% of the targets in the sample were larger than $100 million, while 11% were larger than $500 million by market capitalisation. Table 3 lists the top three creeping acquisitions in the sample by their consideration value.

The second most expensive transaction in the sample was Tata Steel’s creeping acquisition of Riversdale Mining. In July 2009, Tata Steel began purchasing shares in Riversdale at a rate of 2.58% every six months. This allowed Tata to acquire 7.75% of Riversdale for $221 million in a little over a year, and made it Riversdale’s largest shareholder. Midway through Tata’s creeping acquisition, Rio Tinto launched a $4 billion takeover bid for Riversdale. Ultimately, under pressure from Tata and another large shareholder, Rio was forced to increase its offer price from $16 per share to $16.50 per share in order to complete the bid. In effect, Tata was able to use the creeping provision to lift its stake in Riversdale and contest the Rio bid — for a profit. After strategically creeping up Riversdale’s register, Tata sold its entire stake in Riversdale for $1.1 billion. For just the shares that Tata had purchased under s 611(9), the sale made it a substantial profit of 49%. Tata’s takeover defence shows that s 611(9) can be strategically valuable outside of the micro-cap segment.

Table 3: Top three creeping acquisitions by value of consideration

|

Acquirer

|

James Packer and Consolidated Press

|

|

Tata Steel Pty Ltd

|

|

Barro Properties Pty Ltd

|

|

Target

|

Crown Ltd

|

|

Riversdale Mining Ltd

|

|

Adelaide Brighton Ltd

|

|

Target market cap ($ m)

|

6,553.00

|

|

1,560.00

|

|

932.00

|

|

Consideration ($ m)

|

755.11

|

|

220.50

|

|

163.64

|

|

Voting power acquired

|

12.59

|

|

7.75

|

|

9.10

|

|

Creep intensity (%)

|

1.80

|

|

2.58

|

|

0.57

|

|

Pre-acquisition voting power (%)

|

37.02

|

|

19.38

|

|

19.90

|

|

Post-acquisition voting power (%)

|

51.01

|

|

27.14

|

|

30.40

|

Table 4 shows that over our sample period just 11% of the creeping acquisitions occurred solely through off-market purchases. Most acquisitions occurred onmarket, and in the open. The median target size for all off-market purchases was very small at $17–$19 million by market capitalisation. Companies this small generally have highly concentrated ownership and low liquidity, so acquiring even relatively small stakes entails direct dealings with individual owners. Arguably, high ownership concentration should mitigate concerns about creeping acquirers achieving control without due notice. Clerc et al contend that the rules on creeping in France, Greece, the UK and Ireland reflect the distinctive features of each market.[44] France and Greece allow creeping takeovers ostensibly because the prevalence of large blockholders means power is already concentrated.

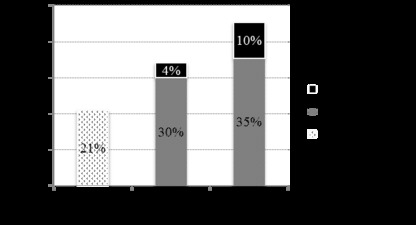

A further 18% of the acquisitions in the sample involved hybrid (ie, on- and off-market) purchases. Creeping acquisitions combining on- and off-market channels involved purchases of voting power far above average. The median percentage increase in voting power is 5.80%. Hybrid acquisitions combine with ‘pure’ off-market acquisitions to make up 29% of the sample — which, by way of comparison, is no less than 10% of the number of successful takeovers and schemes that occurred between 2003 and 2013.[45]

Table 4: Creeping acquisitions by method (median results)

|

|

On-market

|

|

Off-market

|

|

On- and off-market

|

|

Number

|

172

|

|

27

|

|

43

|

|

Target market cap ($ m)

|

41

|

|

19

|

|

17

|

|

Consideration ($ m)

|

1.42

|

|

1.00

|

|

1.17

|

|

Voting power acquired (%)

|

2.82

|

|

1.70

|

|

5.30

|

|

Creep intensity (%)

|

1.42

|

|

1.44

|

|

1.41

|

To measure the final level of voting power reached by a creeping acquirer, we need to be reasonably certain that its program of acquisition has ended. To this end, we eliminated any acquisition that included a ‘change in substantial shareholding’ notice lodged after 2011 so as to reduce the odds that any creeping acquisition we reviewed was incomplete and continued past the time of writing.[46] This left us with 189 observations.

We rounded down the level of voting power reached by an acquirer under s 611(9) to the nearest per cent because there are threshold levels of voting power that provide the holder with disproportionate influence. For instance, a 90% holding is required to commence compulsory acquisition under s 664A of the Corporations Act, so it is plausible that holding 90% is significantly more valuable than an 89% holding, other things being equal. Hence, for example, when assessing the final level of voting power that an acquirer reached using s 611(9), an 89.9% holding was rounded down to 89%, rather than up to 90%.

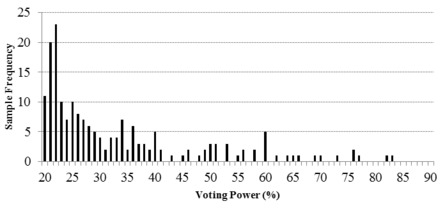

The 20% takeover threshold may have been a natural holding for some shareholders if they wished to maximise their investment exposure without launching a takeover bid. However, statistical tests suggested that the distribution of voting power acquired was not random and that creeping acquisitions were undertaken with a view to acquiring influence, if not outright control.[47]

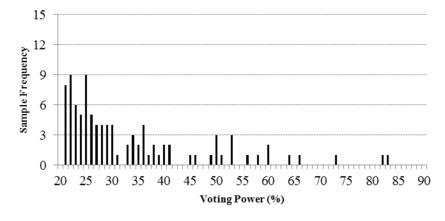

Figure 3 shows most acquirers ended with around 30% voting power. The Eggleston Committee Second Interim Report recognised that ‘[i]n the case of a company with large numbers of small shareholders it is unlikely that any one shareholder would need to control as much as one-third of the voting power to gain control of the company’.[48] Consistent with this point, Corporate Governance International Pty Ltd’s 2003 study of 100 ‘widely held’ ASX-listed companies showed that, on average, the holders of only 44% of the shares issued in those companies voted on director-election resolutions.[49] Lamba and Stapledon’s findings lend further support.[50] Their review of 240 ASX-listed companies revealed that only 16% of those companies had a non-institutional investor with a majority stake greater than 50%.[51] This finding implies that, more often than not, holdings below 50% may deliver sufficient control.[52] The mean and median holdings that the creeping acquirers in our study reached were 33.8% and 27.9% respectively. The mean and median levels dropped only slightly to 28.2% and 25.4% conditional on acquirers stopping before they reached a 50% holding.

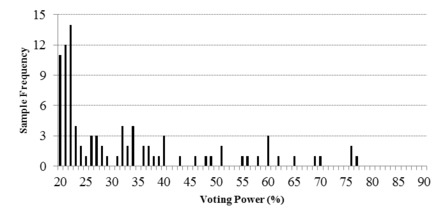

Of the 189 creeping acquirers, there were 92 who lodged just one notice of change of substantial shareholding and 97 that lodged multiple notices. Figure 4 shows that ‘one-off’ acquirers ended up with holdings predominately in the region of 21–2%. After the 22% mark, the stopping pattern for one-off creeping acquisitions became more dispersed.[53] In contrast, Figure 5 shows many acquirers who lodged multiple notices of changes in substantial shareholding were content to stop creeping once they held around 25% voting power. A shareholder with at least 25% of the voting power in a company has the ability to block shareholder resolutions that require 75% or more in assent to pass. Those ‘special’ resolutions are necessary to instigate key strategic developments in a company, like changing a company’s constitution or its name, or entering into a scheme of arrangement.[54] A chi-square test rejected the null hypothesis of no association for multi-notice acquisitions,[55] while the fit tests for Poisson and Negative Binomial distributions were also rejected. [56]

Figure 3: Voting power acquired via creeping

Figure 3 shows hardly any creeping activity ceased at the 75% level, a holding that delivers control of the outcome of special resolutions; and there was no activity at the 90% compulsory acquisition level. The lack of activity around 90% could be because very few full-bids fail close to completion, as shareholders are unlikely to resist an offer at that stage out of a fear of becoming a vulnerable minority shareholder. On this thinking, most bids may either reach compulsory acquisition or fail more substantially — fewer bids might fail just short of 90%.[57] Furthermore, even if some takeovers do fail close to 90%, after being forced to make a full-bid under the equality principle, it may turn out that some bidders do not actually want 100% ownership.

Nonetheless, the lack of creeping activity around 90% does not mean that the creeping provision does not play a role in the final stages of a full-bid.

The availability of s 611(9) of the Corporations Act — as a potential path to acquire sufficient shares to reach a level where compulsory acquisition of outstanding shares is available — ensures that ‘greenmailing’[58] is a lot harder to orchestrate amongst a dispersed group of remaining shareholders.[59]

In addition, it is also possible that a significant controlling stake in one’s target allows an acquirer to exploit other exceptions in s 611 of the Corporations Act to purchase shares. With enough influence, things like rights issues, underwriting agreements and buy-backs could all be used to help a controlling shareholder further increase their holding up to either 75% or 90% without the need for the creeping provision.

Figure 4: Voting power reached — ‘One-off’ acquisitions

Figure 5: Voting power reached — ‘Multi-notice’ acquisitions

From at least as early as Grossman and Hart in 1980,[60] a number of studies have noted that a bid may be more profitable if shares can be purchased stealthily below the takeover threshold without the market knowing that a transaction will soon be announced. If there is no market ‘leakage’ about the bid, it might be possible to acquire a holding below the offer price so that the bidder may ‘gain, either as a buyer that needs to pay a premium for fewer shares or as a losing bidder that sells out at a profit’.[61]

Bulow, Huang and Klemperer,[62] and Dasgupta and Tsui,[63] used game theory to find that a bidder with a larger shareholding in its target than its competitor has a greater probability of winning an auction. This analysis is confirmed by Betton and Eckbo, who reviewed US tender offers made between 1971 and 1990 and found that the larger a bidder’s pre-bid shareholding, the lower the level of both competition and management resistance.[64]

While theory and empirical findings on toeholds indicate creeping acquisitions may be springboards for takeover bids, Canil and Rosser contended the value of a pre-bid holding in Australia is ‘doubtful’ because competing bidders may be able to acquire toeholds of a similar size given Australia’s relatively low takeover threshold of 20%.[65] Consistent with this proposition, Rossi and Volpin,[66] and Bugeja and da Silva Rosa,[67] reported that Australia’s takeover threshold is associated with a lower level of M&A activity relative to the UK, which has a similar takeover code, but a higher threshold of 30%.

Given the above, it is arguable that creeping acquisitions facilitate more takeover bids because they may be used to obtain pre-bid holdings above 20% that lower the costs of making a takeover bid. Aspris, Foley and Frino found that in a sample of 170 takeovers between 2000 and 2009, in which the bidders initially held less than 50% of their targets, 35% of those bidders had a holding above 20%.[68] The following analysis builds on the authors’ earlier work.

Table 5 describes the subset of creeping acquisitions in the sample that occurred either, one year before a takeover or scheme was announced, or one year after a takeover or scheme closed.[69] Thirty-four creeping acquisitions, or approximately 14% of the acquisitions in the sample, were made in conjunction with a takeover or scheme. The low percentage understates the economic significance of the acquisitions. The targets in this subset are much larger than those in the whole sample, with median market capitalisations of $104 million for pre-takeover acquisitions and $85 million for post-takeover acquisitions, as compared to $35 million in the whole sample. The eight post-takeover acquirers obtained a median increase of 5.04% of the voting power in their targets and crept at a rate of 1.87% every six months. The post-takeover acquirers finished with close to majority control of their targets on average, with a median final shareholding of approximately 46%.

Table 5: Traditional takeovers

|

|

|

Mean

|

|

Median

|

|

Standard deviation

|

|

|

Number of pre-takeover acquisitions

|

26

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Target market cap ($ m)

|

|

365.00

|

|

104.00

|

|

583.1

|

|

|

Post-creeping holding (%)

|

|

37.36

|

|

30.28

|

|

17.45

|

|

|

Voting power acquired (%)

|

|

4.38

|

|

3.42

|

|

2.74

|

|

|

Time creeping before bidding (years)

|

|

1.55

|

|

0.92

|

|

1.66

|

|

|

Creep intensity (%)

|

|

1.80

|

|

1.72

|

|

0.80

|

|

|

|

|

|

|

|

|

|

|

|

Number of post-takeover acquisitions

|

8

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Target market cap ($ m)

|

|

193.75

|

|

85.00

|

|

327.44

|

|

|

Post-creeping holding (%)

|

|

42.97

|

|

45.63

|

|

17.79

|

|

|

Voting power acquired (%):

|

|

4.62

|

|

5.04

|

|

2.52

|

|

|

Creep intensity (%)

|

|

1.76

|

|

1.87

|

|

0.70

|

|

|

|

|

|

|

|

|

|

|

The mean and median sizes of the pre-bid acquisitions were 4.38% and 3.42% respectively. Table 6 breaks the pre-takeover acquirers into ‘one-off’ and ‘multi-notice’ categories, and shows that the ‘one-off’ acquirers in the sub-sample finished purchasing their shares very shortly before announcing their takeovers, only 1.4 to 3.7 months before. There were also 16 multi-notice acquisitions in the sample which were, not surprisingly, much larger than their one-off counterparts, with a mean and median size of 5.70% and 5.18%. Here, the acquirers finished purchasing their shares even closer to their respective takeovers, at 2.2–2.5 months prior to announcement. In both the one-off and multi-notice cases, it appears that s 611(9) of the Corporations Act was wittingly used as a strategic precursor to increase the certainty or profitability of a later takeover bid.

Table 6: Pre-takeover acquisitions (one-off and multi-notice)

|

|

Mean

|

|

Median

|

|

|

One-off

|

|

Multi

|

|

One-off

|

|

Multi

|

|

|

|

|

|

Target market cap ($ m)

|

370.00

|

|

362.00

|

|

81.00

|

|

145.00

|

|

|

Post-creeping holding (%)

|

38.64

|

|

34.40

|

|

34.15

|

|

27.91

|

|

|

Voting power acquired (%)

|

2.17

|

|

5.70

|

|

2.24

|

|

5.18

|

|

|

Time between last purchase and takeover announcement (months)

|

1.42

|

|

2.52

|

|

3.65

|

|

2.18

|

|

|

Creep intensity (%)

|

2.09

|

|

1.62

|

|

2.24

|

|

1.65

|

|

|

|

|

|

|

|

|

|

|

|

|

Multi-notice

|

16 (61.5%)

|

|

|

|

|

|

|

|

|

One-off

|

10 (38.5%)

|

|

|

|

|

|

|

|

The ability to get board seats or make an appointment to the board is a direct measure of influence. We used Morningstar’s DatAnalysis service to find out how many creeping acquirers in our sample of 242 got a seat on their target’s board either before, during or after using s 611(9) of the Corporations Act. If an acquirer had a board seat, we classified them as either ‘personal’ or ‘corporate’.

A ‘corporate’ seat is one where the appointed director either sits on the acquirer’s board, or is employed by the acquiring company (or one of its associates).[70]

A ‘personal’ seat is one where the creeping acquirer is; the director himself or herself; a company that is a trustee for the beneficial director; or a private company in which the director has at least a 30% shareholding.[71]

Figure 6 shows that 14% of the acquirers won board seats in their targets while using s 611(9) of the Corporations Act, or afterwards, and most were corporate appointees. Remarkably, 65% of the creeping acquirers had a board seat before they started purchasing shares. This finding raises questions related to:

(a) insider trading; (b) managerial entrenchment; and (c) the extent the creep provisions are used in conjunction with other exceptions in s 611 to acquire control.

Figure 6: Board seats

In relation to insider trading, research to date indicates directors’ purchases are insignificantly related to future firm performance.[72] However, the lack of association may be due to the notorious difficulties in splitting information-based trading from liquidity-motivated trading.[73] Arguably, directors’ creeping trades are more likely based on strategic information and so easier to differentiate from liquidity-motivated trading. Indeed, 70% of the formal takeovers in our sample involved bidders who had board seats prior to their pre-bid creeping acquisitions.

In relation to entrenchment, Morck, Shleifer and Vishny posit that ‘a manager who controls a substantial fraction of the firm’s equity may have enough voting power or influence ... to guarantee his employment with the firm at an attractive salary’.[74] With ‘effective control, the manager may indulge his preference for non-value-maximising behavior’.[75] Table 7 reveals almost half of the directors in the sample used s 611(9) of the Corporations Act to obtain a personal shareholding inside the 20–25% region of ownership that Morck, Shleifer and Vishny found to be associated with lower firm performance in their study of 371 Fortune 500 companies.[76] However, the target firms in this subset had a median market capitalisation of only $12 million. There is a potential concern that the perquisites the directors are able to secure in these small companies may be much greater than the cost of the equity they purchased.[77]

As most creeping acquirers held board seats in their targets before their purchases, we investigated whether s 611(9) is used in conjunction with the other exceptions to the 20% threshold in s 611 (like buy-backs, underwriting agreements or rights issues). With their voting power and board representation, creeping acquirers could influence their targets to engage in buy-backs, rights issues or underwriting agreements that may further facilitate an acquisition of control.

There is an inherent tension between facilitating capital raisings and increasing the probability of abuse of the control ‘gateways’ in s 611. On the one hand, Philip notes that without the permission of a gateway:

substantial rights issues would be impossible for many companies due to the inherent uncertainty surrounding whether major shareholders could support the issue. This would, in turn, severely restrict the company’s ability to raise fresh equity.[78]

On the other hand, however, when there is a substantial shortfall in a rights issue, that issue may lead to an increase in voting power for a major supporting shareholder. Therefore, Philip highlights that ‘regulators have been keen to ensure that the “gateways” in the legislation to facilitate ... equity raisings are not used as an artifice to deliver control without paying a takeover premium’.[79] Conceivably, that same notion might also apply to buy-backs, which could deliver extra voting power to an abstaining shareholder.

In balancing those competing policy factors, the Takeovers Panel has stated that to prevent a rights issue or underwriting arrangement from giving rise to ‘unacceptable circumstances’, it must be made ‘genuinely accessible’ to all shareholders. This term embodies ‘not just providing an opportunity to participate in the rights issue but ... looking at the likely reaction to the offer of shareholders and other investors and the likely effects of the issue on shareholders and the issuer’.[80] Basically, an issue may be declared ‘unacceptable’ if it is structured in a way that is likely to lead to a shortfall and give a major shareholder control.[81] For instance, an issue may be priced far above market prices so as to deter participation.[82] As Philip succinctly puts it: ‘The Panel derived the principle of genuine accessibility from the Eggleston principle that all persons have a reasonable opportunity to accept the offers [and avoid dilution]’.[83]

Table 7: Creeping acquisitions by directors personally

|

|

|

Mean

|

|

Median

|

|

Standard deviation

|

|

|

Number of acquisitions by directors personally

|

82

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Target market cap ($ m)

|

|

203.00

|

|

12.00

|

|

805.65

|

|

|

Pre-creeping holding (%)

|

|

29.46

|

|

23.03

|

|

11.86

|

|

|

Post-creeping holding (%)

|

|

33.88

|

|

29.67

|

|

12.90

|

|

|

Voting power acquired (%)

|

|

4.14

|

|

2.97

|

|

3.73

|

|

|

Creep intensity (%)

|

|

1.64

|

|

1.41

|

|

0.92

|

|

|

|

|

|

|

|

|

|

|

|

Number ending in 20–25%

|

33

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Target market cap ($ m)

|

|

33.00

|

|

8.00

|

|

60.44

|

|

|

Voting power acquired (%)

|

|

2.72

|

|

2.39

|

|

1.79

|

|

|

Creep intensity (%)

|

|

1.53

|

|

1.23

|

|

0.87

|

|

In balancing those competing policy factors, the Takeovers Panel has stated that to prevent a rights issue or underwriting arrangement from giving rise to ‘unacceptable circumstances’, it must be made ‘genuinely accessible’ to all shareholders. This term embodies ‘not just providing an opportunity to participate in the rights issue but ... looking at the likely reaction to the offer of shareholders and other investors and the likely effects of the issue on shareholders and the issuer’.[84] Basically, an issue may be declared ‘unacceptable’ if it is structured in a way that is likely to lead to a shortfall and give a major shareholder control.[85] For instance, an issue may be priced far above market prices so as to deter participation.[86] As Philip succinctly puts it: ‘The Panel derived the principle of genuine accessibility from the Eggleston principle that all persons have a reasonable opportunity to accept the offers [and avoid dilution]’.[87]

To determine whether creeping acquisitions were made in conjunction with other exceptions in s 611 of the Corporations Act, we rely on the presumption that a creeping acquirer must have relied on another gateway in s 611 if the voting power that he or she acquired under s 611(9) was less than the difference between his or her pre-creeping and post-creeping shareholdings. Conversely, any acquisition that was larger than the above difference implies that the acquirer either sold down their stake during the time that they were purchasing shares under s 611(9) or they were diluted. There is one caveat to this approach: it recognises if other exceptions in s 611 were used to purchase shares in between the changes in shareholding notices that were lodged by creeping acquirers — but it neglects other exceptions if they were used before or after creeping acquisitions.

Table 8 shows that approximately 18% of the acquisitions in the sample were made in conjunction with another exception in s 611 of the Corporations Act. Noticeably, the voting power that was purchased by the creeping acquirers under s 611(9) in this subset was considerably high at 5.62–6.88%. But their total size (ie, the difference in their pre and post-creeping holdings) was remarkable — it was far greater at 8.56–13.05% — with an effective acquisition rate of 2–2.4% every six months. In combining their use of the creeping provision with the other gateways in s 611, it seems that these acquirers were willing to pursue several means to increase their voting power.

At the other end of the spectrum, 14% of the acquirers in the sample used s 611(9) of the Corporations Act to increase their voting power before and after dilutive events or share sales. They too comprised large acquisitions, with a mean and median size of 6.89% and 5.87% respectively. Perhaps here the creeping provision is used to counter the dilutive effects of capital raisings that are instigated by larger shareholders.

Table 8: Creeping acquisitions and other exceptions

|

|

|

Mean

|

|

Median

|

|

Standard deviation

|

|

|

Number of

‘Pure’ creeping Acquisitions

|

166

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Target market cap ($ m)

|

|

166.00

|

|

29.00

|

|

430.65

|

|

|

Voting power acquired (%)

|

|

2.80

|

|

2.29

|

|

2.29

|

|

|

Creep intensity (%)

|

|

1.79

|

|

1.61

|

|

0.83

|

|

|

|

|

|

|

|

|

|

|

|

Number of acquisitions with other exceptions

|

43

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Target market cap ($ m)

|

|

417.00

|

|

51.00

|

|

1084.59

|

|

|

Voting power acquired (%)

|

|

6.88

|

|

5.62

|

|

3.64

|

|

|

Total voting power acquired (%)

|

|

13.05

|

|

8.56

|

|

11.83

|

|

|

Creep intensity (%)

|

|

1.48

|

|

1.29

|

|

0.91

|

|

|

Effective intensity (%)

|

|

2.40

|

|

2.00

|

|

1.36

|

|

|

|

|

|

|

|

|

|

|

|

Number of acquisitions with dilution or sales

|

33

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Target market cap ($ m)

|

|

115.00

|

|

32.00

|

|

198.68

|

|

|

Voting power acquired (%)

|

|

6.89

|

|

5.87

|

|

3.35

|

|

|

Net increase (%)

|

|

3.12

|

|

3.09

|

|

5.41

|

|

|

Creep intensity (%)

|

|

1.48

|

|

1.11

|

|

0.87

|

|

|

Net intensity (%)

|

|

0.79

|

|

0.81

|

|

1.07

|

|

Creeping acquisitions have been allowed in Australia for well over 30 years. Our findings on their incidence and characteristics over the ten-year period spanning April 2003 through to April 2013 facilitate a more nuanced understanding of how creeping acquisitions align (or not) with the ostensible objectives of Australian takeover regulation.

Creeping acquisitions are more ubiquitous than many commentators believe. Our findings suggest resort to creeping as an alternative to formal takeover bids is a function of the cost of delaying a transfer in control or influence; in boom times, the incidence of formal takeover bids increases while that of creeping acquisitions decreases and vice versa in recessionary periods. To our knowledge, the impact on equity market liquidity of banning creeping acquisitions has never been canvassed.

Treasury is among those that have expressed concern about the potential for creeping acquirers to achieve control without paying a premium to target shareholders.[88] This perspective presumes more certainty about the acquirer’s intent than is arguably reasonable. The Takeovers Panel, among others, has argued the importance of creeping acquisitions being gradual and open to comply with the spirit of the Eggleston Principles.[89] It is ironic then that calls to revoke creeping acquisitions tend to be prompted by instances where a prominent acquirer makes a gradual, open and seemingly inexorable move to achieve control of their target.

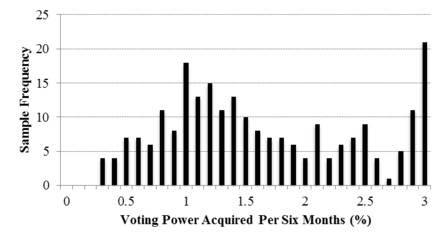

Our results indicate gradual acquisitions of voting power are the norm. Acquirers do not typically hit the limit of 3% every six months. Just 84 (ie, 35%) out of 242 creeping acquirers in our sample purchased shares at a rate higher than 2% every six months.[90] One caveat: increases in voting power from share placements have been omitted from our study because both the creeping ‘gateway’ and also s 611(7) of the Corporations Act — shareholder approval — may justify them. Placements are used to quickly raise cash from large shareholders, so an amendment to s 611(9) to lower the creeping maximum to below 3% may reduce the capital-raising ability of some companies if they rely on the creeping provision to be allowed to make placements to their large shareholders.[91]

Although the pace of creeping is typically slow, we found acquirers who rely on s 611(9) of the Corporations Act achieve substantial increases in voting power: 55% of our sample acquirers lodged multiple notices, and they acquired 5.87% of their target’s voting power on average.

Figure 7: Creep intensity

The control or influence achieved by creeping acquirers can be expected to vary considerably. Peden observes,

[d]epending upon the dispersal of the existing shares, the acquisition of forty, twenty-five or even fifteen per cent of the shares may confer effective de facto control, and such an acquisition will be very much cheaper than the purchase of 100 per cent of the shares.[92]

Figure 4 shows most acquirers in our sample stopped acquiring shares when their holdings were well below 50%, although a significant proportion used s 611(9) even when they had acquired well over 50% voting power.

Analysis of influence gained from creeping must account for the disproportionate leverage a shareholder achieves when they pass particular voting power thresholds. A topical example is the ‘twostrikes rule’.[93] A company incurs a ‘strike’ if at least 25% of shareholder votes cast are against a company’s remuneration report. If a company records a strike at two consecutive Annual General Meetings (‘AGMs’), its shareholders must also vote on a ‘spill resolution’, which can ultimately lead to a board spill.[94] Notwithstanding Parliament’s intention, shareholder activists may use the twostrikes rule to take action against non-remuneration-based issues and thereby influence a company’s direction.[95] This practicality makes obtaining 25% of the voting power in a company disproportionately valuable and may, at least in part, motivate creeping acquisitions made after 2011, when the twostrikes rule was enacted.

Off-market purchases and creeping by board members are aspects of creeping acquisitions that arguably violate the principle of equality of target shareholders’ opportunity to benefit from a transfer of control. However, prohibiting off-market purchases and/or curtailing board members’ ability to participate in creeping acquisitions may damage target firm shareholders. We found the targets of most off-market purchases are very small firms (by market capitalisation). Small firms typically have highly concentrated shareholdings and so prohibiting creeping acquisitions may substantially lower liquidity in the market for their shares. Clerc et al note that different regulatory approaches to creeping takeovers across European countries can be justified on the basis of differences in ownership concentration.[96]

We close by noting that discussions on creeping acquisitions in Australia have typically relied on stylised facts about the incidence and characteristics of creeping acquirers and their targets that have not been empirically verified. This is probably due to the challenges in collecting and analysing the requisite data to test propositions about the market for creeping acquisitions. Our review of over 50 000 notices of changes in substantial shareholdings made over the ten-year period April 2003 to April 2013 provides the first largescale survey of creeping acquisitions. The market for creeping acquisitions is economically significant and operates largely consistent with the Eggleston Principles. We find no pressing reason for the regulation of creeping acquisitions to be modified on either equity or efficiency grounds.

[∗] Winthrop Professor, UWA Business School, The University of Western Australia. Email: ray.dasilvarosa@uwa.edu.au.

[†] B Comm (Hons I) LLB; Analyst, Walk Free. This article is based on Michael’s honours thesis at the University of Western Australia (supervised by Raymond da Silva and David Yermack).

Email: mkingsbury@walkfree.org.

[‡] Albert Fingerhut Professor of Finance and Business Transformation, Leonard N Stern School of Business, New York University. Email: dyermack@stern.nyu.edu.

We thank Mark Paganin of Clayton Utz and Justin Mannolini of Macquarie Capital for helpful discussions. We lay claim to all errors.

[1] Australian Government Treasury (‘Treasury’), ‘Takeovers Issues — Treasury Scoping Paper’ (2012) <http://www.treasury.gov.au/PublicationsAndMedia/Publications/2012/Takeovers-issues> .

[2] Companies (Acquisition of Shares) Act 1980 (Cth) s 15. This provision replaced s 180C(2)(b) and s 180C(7) of the Uniform Companies Acts 1961–1962 (State Legislative Scheme), which allowed prospective acquirers to purchase an unlimited number of shares from up to three members every four months or at any time in the ‘ordinary course of trading on the stock exchange’..

[3] Commonwealth, Parliamentary Debates, House of Representatives, 16 April 1980, 1815 (Ray Braithwaite). Note, however, that legislative intention should not be determined solely from the subjective views of Parliament; as the majority of the High Court espoused in Alcan — ‘the task of statutory construction must begin with a consideration of the text itself’: Alcan (NT) Alumina Pty Ltd v Commissioner of Territory Revenue [2009] HCA 41; (2009) 239 CLR 27, 46 [47].

[4] Michael Smith, ‘Two Sides to “Creep” Reform’, The Australian Financial Review (Melbourne), 17 July 2012, 23.

[5] Pursuant to the Corporations Act s 606.

[6] Commonwealth, Company Law Advisory Committee to the Standing Committee of Attorneys-General: Second Interim Report, Parl Paper No 43 (1969) [4]–[5] (‘Eggleston Committee Second Interim Report’); see also the Corporations Act ss 602, 611(1), 611(17), 618, 623, 636.

[7] Under the Corporations Act s 671B, a creeping acquirer only needs to lodge a notice of a change in its substantial shareholding when it increases its voting power by 1% in its target.

[8] Corporations Act s 611(9).

[9] Treasury, above n 1.

[10] Eggleston Committee Second Interim Report, above n 6, [16].

[11] The Takeovers Panel was established under Australian Securities and Investments Commission Act 1989 (Cth) s 171.

[12] Corporations Act ss 9, 657A; the Takeovers Panel may make a ‘remedial’ order that may, inter alia, void a transfer or issue of shares. The following statement by Kirby J in AG (Cth) v Alinta Ltd (2008) 233 CLR 542, 562 [45] describes the Federal Parliament’s view of the nature and objectives of the Takeovers Panel:

Certainly, it was open to the Federal Parliament to conclude that the nature of takeovers disputes was such that they required, ordinarily, prompt resolution by decision-makers who enjoyed substantial commercial experience and could look not only at the letter of the Act but also at its spirit, and reach outcomes according to considerations of practicality, policy, economic impact, commercial and market factors and the public interest.

[13] Corporations Act ss 602, 636.

[15] Benedict Sheehy, ‘Australia’s Eggleston Principles in Takeover Law: Social and Economic Sense?’ (2004) 17 Australian Journal of Corporate Law 218, 222 with the author referring to Corporations Act s 602(a).

[16] See Elaine Hutson, ‘Regulation of Corporate Control in Australia: A Historical Perspective’ [1998] CanterLawRw 8; (1998) 7 Canterbury Law Review 102, 117 where the author cites an anonymous Sydney lawyer who, as early as 1983, opined: ‘As to the Eggleston Committee’s view of takeovers, the legislation has been biased so much to the protection of the target company in a takeover that it serves only to entrench inefficient managements, to the costs of their shareholders’.

[17] Frank H Easterbrook and Daniel R Fischel, ‘Corporate Control Transactions’ (1982) 91(4) Yale Law Journal 698, 709–10.

[18] David Herro, a large US-based investor in New Zealand-listed brewer Lion Nathan, warned that regulations that allowed Kirin Brewery to take over Lion Nathan by offering a higher price to the controlling shareholders ran the risk of scaring off foreign investors from New Zealand: David G Herro, ‘Untethered Lion Scares Foreign Investors’, New Zealand Herald (New Zealand), 13 May 1998, E2. Treasury has also recognised the trade-off between promoting market confidence and liquidity and providing incentives for information search. It has stated that: ‘without the investor protection provided by the equal opportunity principle, it may be less likely that smaller investors would invest directly in the market, which could affect market liquidity and confidence’. Later in the same article, it is acknowledged that ‘market inefficiencies arising from the current law may add costs to takeovers’: Treasury, Takeovers — Corporate Control: A Better Environment for Productive Investment, Corporate Law Economic Reform Program, Proposals for Reform: Paper No 4, 1997, 14, 16 (‘CLERP Paper 4’). See also Amar Bhide, ‘The Hidden Costs of Stock Market Liquidity’ (1993) 34 Journal of Financial Economics 31, 31.

[19] Australia Securities and Investments Commission, Regulatory Guide 6 — Takeovers: Exceptions to the General Prohibition, June 2013, 18, 21 (‘ASIC Regulatory Guide 6’). ASIC has suggested that it may only apply to seek ‘unacceptable circumstances’ if a creeping acquirer fails to abide by its substantial shareholder disclosure requirements: ASIC Regulatory Guide 6, 20 [RG 6.57]. Practically speaking, this view is supported by the premise that any ‘change in control’ will occur ‘slowly enough for those affected to make informed decisions in response’: ASIC Regulatory Guide 6, 18 [RG 6.48]. Essentially, ASIC believes that target shareholders will have enough time to inform themselves about the merits of a change in control, and also an equal opportunity to liquidate their investments during the acquisition period.

[20] [2012] ATP 10 (27 July 2012), 15 [100].

[21] James Graham, ‘How to Drive a Horse and Cart through the New Takeover Code’, The Australian Financial Review (Australia), 17 January 1979, 24.

[22] The City Code on Takeovers and Mergers (UK) r 5.1(b) (‘City Code’).

[23] L Fitzgibbons, ‘Emerson’s Astec Bid Prompts to Ban “Creeping” Takeovers’, The Lawyer (online), 6 September 1998 <http://www.thelawyer.com/emerson039s-astec-bid-prompts-plan-to-ban-creeping039-takeovers/92206.article> .

[24] Rodd Levy, ‘Time to Axe the 3pc Creep Rule’, The Australian Financial Review (Melbourne), 2 July 2012, 43. ASIC has highlighted a number of areas where it is concerned that the current laws may need modernising (see Treasury, above n 1). One basis for ongoing review and ostensible modernisation of the law on creeping acquisitions is changing market conditions. Clerc et al, for example, contend that the rules on creeping in France, Greece, the UK and Ireland reflect the distinctive features of each market: Christophe Clerc et al, A Legal and Economic Assessment of European Takeover Regulation (Centre for European Policy Studies, 2012) 56. France and Greece allow creeping takeovers ostensibly because the prevalence of large blockholders means power is already concentrated. In contrast, more diffuse shareholding in the UK and Ireland means that small increases in shareholding can potentially result in a transfer of control and so creeping is effectively prohibited. It is arguable that increasingly widespread shareholding in Australia justifies greater restrictions on creeping acquisitions. In the US, creeping is unimpeded; investors are allowed to accumulate sufficient shares in a target to achieve control without a mandatory bid for remaining shares.

[25] Companies and Securities Law Review Committee, Partial Takeover Bids, Report No 2 (1985) appendix [17] (‘CSLRC 1985 Report’).

[26] Adolf A Berle and Gardiner C Means, The Modern Corporation and Private Property (Macmillan, 1933) 244, cited and discussed in Henry G Manne, ‘Mergers and the Market for Corporate Control’ (1965) 73(2) Journal of Political Economy 110, 116.

[27] See for example Short v Treasury Commissioners [1948] AC 534; Perlman v Feldmann 219 F 2d 172 (2nd Cir, 1955).

[28] Keith Dowding, Power (University of Minnesota Press and Open University Press, 1996).

[29] Treasury, above n 1, 2.

[30] Andrei Shleifer and Robert W Vishny, ‘Value Maximization and the Acquisition Process’ (1988) 2(1) Journal of Economic Perspectives 7.

[31] Shleifer and Vishny make this argument in discussing the claim that shareholders have the property right to all the firm’s cash flows not allocated by an explicit contract: ibid 16.

[32] Luigi Zingales, ‘What Determines the Value of Corporate Votes?’ (1995) 110(4) The Quarterly Journal of Economics 1047.

[33] Ibid.

[34] Stephen Mayne, ‘Mayne: How to Reform Australia’s Takeover Laws’, Crikey (online),

10 July 2012 <http://www.crikey.com.au/2012/07/10/mayne-how-to-reform-australias-takeover-laws/?wpmp_switcher=mobile & wpmp_tp=1> .