Sydney Law Review

|

|

Home

| Databases

| WorldLII

| Search

| Feedback

Sydney Law Review |

|

Australia’s Position on Investor–State Dispute Settlement:

Fruit of a Poisonous Tree or a Few Rotten Apples?

Kyle Dylan Dickson-Smith[∗] and Bryan Mercurio[†]

Abstract

This article critically analyses the methodology and substantive basis of Australia’s initial rejection of, and subsequent ambivalence towards, investor–State dispute settlement (‘ISDS’) mechanisms contained in international investment agreements. The analysis focuses on the Australian Government Trade Policy Statement of 2011, as well as the 2010 and 2015 reports of the Australian Productivity Commission that largely informed the conclusions of the Trade Policy Statement. The article reveals that Australia’s analysis was incomplete and lacking meaningful discourse on the general concerns and benefits of ISDS in light of Australia’s regional relationships and the global political economy. Consequently, an adequate debate on the virtues of ISDS has yet to take place in Australia. In the absence of a clear and consistent investment policy, this article provides guidance for Australia’s future policy, such as threshold criteria for the inclusion of ISDS and a model investment treaty. With the European Union and United States expressing dissatisfaction with the present system of ISDS, this article is timely and has broad relevance.

Australia is a lucky country run mainly by second-rate people who share its luck.[1]

The ‘lucky country’ phrase entered, and remained, in the Australian vernacular as a term of endearment, depicting Australia as a country rich in natural resources and prosperity, geographically distant from global problems and, therefore, a great place to migrate or invest. Yet, unknown to most, Horne’s depiction of Australia as the ‘lucky country’ was actually describing a political-legal system largely guided by luck, rather than guided by proactive governance that capitalises on Australia’s underlying economic and legal advantages.[2]

Much has changed in the political-legal system and in Australia more generally since 1964, but this article addresses whether Australia has returned to ‘second rate’ governance whereby economic prosperity is the result not of foresight and planning, but of luck. This certainly appears to be the case behind the Australian Government’s curious policy on international investment and, in particular, investor–State dispute settlement (‘ISDS’). A common feature of international investment agreements,[3] ISDS is a mechanism that allows nationals of a party to an investment agreement to take direct legal action against the counterparty host State for breaches of that agreement. If successful, the host State could be liable for monetary damages payable directly to the investor.

Until 2011, Australia included ISDS in almost all of its investment agreements as a matter of course, with little discussion or debate. One notable exception is the Australia–United States Free Trade Agreement (‘AUSFTA’),[4] which excluded ISDS at the request of Australia.[5] This exclusion by the conservative Howard Government perhaps planted the seed for the later left-leaning Gillard Government’s Trade Policy Statement, which, inter alia, ostensibly declared that ISDS would no longer be included in Australian investment agreements.[6] In so doing, Australia became one of the few countries to reject ISDS in its investment agreements. Other states such as Ecuador, Bolivia, Venezuela and later Indonesia and South Africa clearly set out their bases for rejecting ISDS.[7] However, Australia’s rejection was not accompanied by detailed or clear rationale. Instead, the Trade Policy Statement left unstated whether the rejection was based on specific institutional or systemic concerns, or simply as part of a general apprehension with the international investment regime. Since 2011, Australia’s position on ISDS has again shifted, multiple times.

Australia included ISDS in all of its 21 bilateral investment treaties (‘BITs’) and most free trade agreements (‘FTAs’) entered into between 1988–2005 (over the Hawke and Keating Labor Governments and Howard Liberal Government), before being omitted by the Gillard Labor Government in FTAs with New Zealand (2010)[8] and Malaysia (2012).[9] The Abbott Liberal-led Government then included ISDS in trade agreements with Korea (2014),[10] the Association of South East Asian Nations (‘ASEAN’) (2014)[11] and China (2015),[12] but not in the FTA with Japan (2014).[13] The recent Government’s ‘case-by-case approach’[14] could very well be reasoned and rationalised, but such repeated shifts do beg the question whether Australia has been guided by any overarching theoretical principles or whether these shifts are simply the result of a schizophrenic policy from successive governments. What is clear is that a case-by-case approach without any underlying guiding principles inevitably leads to confusion and uncertainty in any subsequent negotiations.

The objective of this article is to critically analyse the basis for Australia’s rejection of, and subsequent ambivalence towards, ISDS in the context of its regional relationships and the global political economy. The Australian Productivity Commission reports in 2010 and 2015 largely influenced and informed the conclusions of the Trade Policy Statement.[15] However, even a cursory evaluation of the Trade Policy Statement, as well as those reports, reveals incomplete analysis of the general (global) concerns and a summary dismissal of the benefits (both in general terms and to Australian investors) of ISDS. Consequently, an adequate debate as to the merits of ISDS has yet to take place by the Australian Government.

The topic of this article is apt in light of the most recent developments in Europe and the United States (‘US’) questioning the merits of ISDS.[16] Further, the effects of the June 2016 ‘Brexit’ vote (in favour of the United Kingdom withdrawal from the European Union (‘EU’)) have, inter alia, prompted discussions as to a potential FTA between Australia and the United Kingdom.[17] In addition, an Australian Senate Committee inquiry pertaining to the ratification and implementation of the recently signed Comprehensive and Progressive Agreement for Trans-Pacific Partnership (‘TPP-11’), which includes 10 other partner countries, remains ongoing.[18] Accordingly, this discussion may well shape Australia’s approach in other ongoing negotiations, such as with Indonesia, India and the Chinaled Regional Comprehensive Economic Partnership.[19]

This article is divided into four parts: Part I briefly describes the nature and purpose of ISDS before reviewing its criticisms and benefits. This part addresses the question as to whether states predominantly include ISDS in investment agreements to attract investment, protect their investors overseas or as a response to the greater competitive pressure within the global political economy. Part II outlines Australia’s historical approaches to ISDS, with reference to the aforementioned 2010 and 2015 Productivity Commission reports. This is contextualised against regional (historical and anticipated) trends of ISDS practice. Part III provides a critical analysis of the basis for Australia’s ISDS policy and also discusses the implications in light of Australia’s competitiveness and involvement in the regional economic community. The Part concludes that it is not in Australia’s interest to reject ISDS unless and until a rational basis to do so emerges. Finally, Part IV provides a series of practical reform measures which address both substantive and procedural protections, and further suggests rational guidelines for future policymaking. It contrasts these suggested reforms with those adopted by other states and economies, and specifically draws on existing proposals in the Transatlantic Trade and Investment Partnership (‘TTIP’) negotiations between the US and the EU, as well as the recently signed Comprehensive Economic and Trade Agreement (‘CETA’) between the EU and Canada.[20]

The article concludes with a call for a consistent and principled, but flexible, policy that encapsulates both Australia’s immediate investment needs and long-term prospects within the international investment regime. It is argued that such a policy, complemented with a model BIT,[21] will facilitate efficiency and predictability throughout the treaty negotiation and implementation process.

Before analysing how the Australian Government and the Productivity Commission evaluated the implications of ISDS, it is necessary to first briefly discuss the general purpose and utility of ISDS within the context of the international investment regime. It is also relevant to survey some of the general (global) concerns of ISDS, both to provide context and to assist in the assessment of whether the Australian Government and Productivity Commission’s analyses were conducted meaningfully, fairly and comprehensively.

Countries typically enter into investment treaties for one or more of three reasons: (1) to protect the investments of nationals in the territory of the counterparty; (2) to stimulate inbound foreign direct investment (‘FDI’); and, more generally, (3) to facilitate investment liberalisation. In regards to the third reason, liberalisation involves the removal of restrictions or barriers to entry of foreign companies into host countries, such as opening up the financial structure of a country to market forces, and removing governmental control. Often, it is easier and more politically palatable to liberalise investment (and trade) through an international agreement, rather than unilaterally.[22] Among other factors, one of the general macroeconomic advantages of investment agreements is enhanced competition and consequential improved dynamic efficiency.[23]

ISDS provisions are designed to facilitate the objective of the underlying investment agreement to encourage investment flows by providing procedural recourse for the enforcement of substantive investor protections. ISDS, complemented with protections against discriminatory or unfair government measures, provides a direct mechanism to protect such investments without governmental action or consent by the investor’s home State. Viewed from this perspective, ISDS removes a specific behind-the-border barrier for foreign investors; namely, ineffective judicial or administrative decision-making in the host State.

While the underlying purpose of an investment policy is to reduce behind-the-border barriers in order to attract the flow of capital into a signatory’s territory, it remains debatable whether ISDS actually increases FDI flows and empirical evidence is equivocal on this point.[24] This lack of precision is not surprising given how difficult it is to isolate the direct effects on FDI of investment agreements and ISDS from other factors that influence investment, such as improvements in technology, a general expansion in trade, inflation, currency fluctuation, economic growth or a range of other domestic developments.

Another reason why states utilise ISDS is based on the global political economy and the competitive ‘contagion’ effect created by bilateral arrangements.[25] Simply stated, the increase of bilateral and regional FTAs is purported to create a self-reinforcing, or contagious, process that compels other states to follow and increase the standards of protections in investment agreements in order to remain competitive and attract FDI.[26]

The question for this discussion is whether Australia’s policy towards investment protection, particularly for ISDS, considered these overall factors and concerns. In other words, has Australia considered the literature and broader debate when formulating its investment policy? While it is beyond the scope of this article to compare the advantages of arbitration with local judicial processes,[27] given Australia’s rejection of ISDS in 2011 it is worth reviewing the criticisms of the system before proceeding.

The ISDS discussion exists along several lines of debate, which could perhaps be placed on a scale of the greatest potential ramifications to the least. The first line is whether agreements with ISDS equally distribute benefits to all states and facilitate a fair global governance system. The second line is whether the underlying agreement should grant any procedural rights to investors in ISDS. The third addresses the scope of substantive protections subject to ISDS. The fourth, and more nuanced debate, is based on the forum — whether ISDS procedural rights should be granted through arbitration or domestic courts, or whether investment agreements should provide the investor with a choice of forum. These various lines of debate are interrelated and collectively considered when states decide whether to include or exclude ISDS, to cover greater or fewer key investor protections, and to provide for ISDS with arbitration in addition to, or in lieu of, local court proceedings.

Most criticisms of ISDS relate to legitimacy. As it is beyond the scope of this article to analyse each of these in any depth, these criticisms have been reproduced in the Appendix to this article, with a description as to whether these have been considered by the Australian Government. However, an overall description of the general criticisms can be synthesised as follows:

1. Treaty interpretations by tribunals are often conflicting and the system does not allow for appeals.

2. ISDS unduly restricts states from exercising their traditional sovereign right to protect health, environment and culture, and thus leads to regulatory chill and effectively removes the democratic political process of public/parliamentary debate.

3. ISDS provides asymmetrical procedural rights to investors (but not states), giving exclusive standing to corporations, and creates unique legal norms in favour of multinational enterprises that is fragmented from, and thus left ‘unchecked’ by, other international legal norms, such as international human rights, Indigenous rights,[28] environmental law and (to a lesser extent) trade law.[29] These issues are compounded by agreements and tribunals refusing to grant standing to interested and affected parties or the right of audience through amicus curiae submissions.[30]

4. Substantive investor protections,[31] exceptions[32] and arbitral interpretations[33] are in large part skewed by Western (namely European and American) traditions, without being ‘contextualised’ for the legal regimes of developing states.

Once again, the key question for this article is the extent to which the Australian Government, in its blanket rejection of ISDS in 2011, relied on any of this general discourse and whether it disproportionally attributed excess or little weight to these factors. The remaining sections will evaluate, with this framework in mind, the basis for Australia’s decision with respect to investment agreements and, specifically, ISDS.

The implications of the inclusion/exclusion of ISDS for Australia is best understood from the perspective of appreciating the nation’s political economy, its current and potential position with respect to FDI flows and its treaty practice.[34]

Australia has, for some time, relied on FDI in order to maintain and increase its standard of living. In the words of Australia’s first Minister for Investment:

Since the First Fleet, Australia has been a country unashamedly reliant on foreign investment ... As a big and sparsely populated continent with a thin domestic capital market ... our reliance continues today.[35]

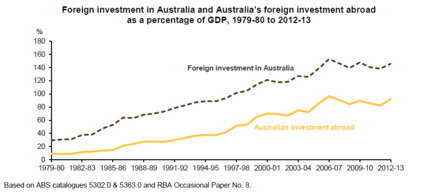

The benefits of FDI to a host State are numerous, and include the provision of capital for economic growth, the creation of employment opportunities, and the increase of productivity and scale of competition between domestic industries, which in turn improves consumer choice.[36] Australia has historically required FDI to employ and expand its population which, in turn, perpetuate further economic growth.[37] Over the period of 1979–2007 (before the Global Financial Crisis), the level of FDI in Australia rose from around 15% of Gross Domestic Product (‘GDP’) to more than 35% (see Figure 1, below).[38] In that same period, the level of Australian FDI abroad rose from less than 5% of GDP to 34.4%.[39]

Notably, the rate of investment between Australia and Asia has more than doubled (in both directions) in the last 10 years.[40] This trend is most noticeable in regards to China. Based on the accumulated volume of FDI between 2005 and 2015, Australia was China’s second largest destination of investment (following the US), totalling US$87.2 billion in 2016 alone.[41] China is now Australia’s largest trading partner and FDI flows have grown significantly in the last decade.[42] However, by international standards, Australia’s level of FDI inflow is not particularly high, accounting for less than 40% of its GDP.[43] Australia could, thus, benefit from further Chinese investment. In terms of Australian FDI, Australia directs more FDI to China, in proportion to many other countries, with significant room for further growth.[44]

Figure 1: Australian Foreign Investment: Inward and abroad as a percentage of

GDP, 1979–80 to 2012–13[45]

Australian investment agreements that omit ISDS are the exception, rather than the norm. Historically, the practice has been to include ISDS and this has been the case for all of Australia’s 21 BITs and all but a select few of its FTAs.[46] Australian trade agreements that exclude ISDS are the Investment Chapter (added in 2011) to Australia’s (first) FTA with New Zealand (1982),[47] the AUSFTA (2004),[48] and FTAs with Malaysia (2012),[49] Japan (2014),[50] and the AANZFTA (2014, only in relation to the obligations between Australia and New Zealand).[51]

Despite a fairly consistent adoption of ISDS, the Government began vocalising concern over ISDS in 2002, when the centre-left Labor Party in opposition successfully campaigned against including ISDS in the AUSFTA.[52] After coming into power in 2007, however, the Labor Party quietly acceded to ISDS in the FTAs signed with Chile (2008)[53] and ASEAN (2009).[54] After expressing ‘serious reservations’ about ISDS in March 2010, the release in 2011 of the Trade Policy Statement firmly staked out the Government’s position:

In the past, Australian Governments have sought the inclusion of investor–State dispute resolution procedures in trade agreements with developing countries at the behest of Australian businesses. The Gillard Government will discontinue this practice.[55]

The Trade Policy Statement was largely based on the 2010 Productivity Commission Report,[56] the recommendations of an independent statutory and advisory body. The Commission’s mandate is to provide the Australian Government with independent and economically rigorous advice,[57] and historically, it has been both rigorous and objective in its evaluation of the Australian policymaking process.

As such, the 2011 Trade Policy Statement’s rejection of ISDS signified a material departure from Australia’s longstanding practice. The position of the Australian Government shifted again just two years later as the newly elected Liberal-led Coalition Government reverted to the previous position of including ISDS on a ‘case-by-case basis’.[58] In line with the Coalition’s ‘pragmatic approach to trade negotiations’,[59] ISDS was included in the 2014 FTAs with Korea (‘KAFTA’)[60] and China (‘ChAFTA’),[61] but not with Japan.

A few months later, in June 2015, the 2015 Productivity Commission Review was released, expressing continued opposition to the negotiation and inclusion of ISDS clauses in investment agreements.[62] Shortly thereafter, Australia and the other 11 parties finalised the text of the Trans-Pacific Partnership (signed in February 2016),[63] and subsequently the TPP-11 (signed in March 2018),[64] both of which contain ISDS as expected. In addition, Australia continues to negotiate the Regional Comprehensive Economic Partnership and other bilateral agreements that are also likely to include ISDS. The willingness to include ISDS more often than not suggests that the Coalition Government and Opposition Labor Party are both more pro-ISDS than the stated policy from 2011 would suggest. Left unaddressed, however, is whether a coherent policy exists with clear aims, objectives and parameters as to when and under what circumstances ISDS is acceptable or unacceptable.

Despite the Australian Government’s foregoing proclamations against ISDS, it is difficult to discern an underlying rationale for Australia’s policy on ISDS. This section analyses whether a historical correlation exists between the inclusion of ISDS and the perceived quality of the foreign State’s legal and judicial system, or similarly, with the host State’s GDP or real and anticipated FDI flows between the counterparty. One would expect that the utility of adopting an ISDS provision between two developed countries would be more nuanced, relative to those between a developed and a less-developed State. Similarly, there would appear to be less potential for Australian investors to use ISDS against a State where there is only a small amount of outbound investment, relative to states with greater FDI outflow (that is both historical FDI flows and potential FDI).

1 Host Legal System

Historically, one can perhaps find a correlation between ISDS and the counterparty’s developmental state and legal system, such that Australian agreements negotiated with less-developed countries include ISDS. Upon further exploration, however, the strength of the correlation weakens. Australia has generally excluded ISDS with developed countries, such as New Zealand, the US and Japan. However, it also excluded ISDS with Malaysia. At the same time, Australia has included ISDS with Singapore (2003), Thailand (2005), Chile (2008), the AANZFTA (2009) and Korea (2014). Countries such as Korea, Chile and Singapore have what would be generally described as developed legal systems, on par with, if not more advanced than, one or more of the countries with which ISDS has been excluded.[65] It does not, therefore, appear that the state of a country’s legal system is a determining factor in whether Australia seeks to include or exclude ISDS.

2 Host State GDP

The same contradictions appear in relation to a country’s overall wealth. Again, Korea, Chile and Singapore are high-income countries. On the other hand, Thailand’s economic development level is equivalent to Malaysia, yet those two countries are treated differently. Moreover, both are members of ASEAN, an agreement in which Australia includes ISDS. The point being, it is clear that level of economic development and GDP does not appear relevant to the decision to include or exclude ISDS.[66]

3 FDI Flows between Counterparties

Looking more closely at the statistics, there does not even appear to be a clear pattern or trend in relation to FDI flows and the inclusion of ISDS. It would appear, however, that Australia includes ISDS provisions in agreements where it is a net FDI-exporter and seeks to exclude such provisions in treaties where it is a net FDI-importer.[67] But, even here, the practice is inconsistent. Australia is a net FDI-exporter (or at least was at the time the relevant agreement was entered into) in relation to Chile and Thailand. However, it is a net FDI-importer in relation to Singapore, Korea, China and most ASEAN countries,[68] yet all of the relevant agreements with these countries include ISDS. This correlation is also imperfect where ISDS has not been included in an agreement. For instance, Australia is a net exporter of FDI with the US and New Zealand (again, at the time the relevant agreement was entered into), and a net importer of FDI from Malaysia and Japan — yet no ISDS is included in any of these treaties.[69]

Parts IV and V of this article will address whether these factors have been, or should be, utilised as official threshold criteria to invoke ISDS and to determine when ISDS should be included and/or placed on the negotiating table.

This Part analyses both the findings and basis of the 2010 and 2015 Productivity Commission reports and the Trade Policy Statement, focusing on the particular framing of the international investment legal regime. This Part also demonstrates that many of the general issues surrounding ISDS, such as those described in Part I, were not addressed and analysed by the Productivity Commission or by the Australian Government in the formulation of its policy. Overall, we find the combined analysis of the Productivity Commission and the Trade Policy Statement to be incomplete and beset with internal contradictions. A summary of our findings is contained in the Appendix to this article.

The Productivity Commission’s basis for rejecting the use of ISDS can be described as: (i) part of its principal approach in rejecting investment agreements; (ii) a specific rejection of the ISDS mechanism; or (iii) both (i) and (ii). Unfortunately, the Commission’s reasoning blurs the issues and leaves the dividing line between (i) and (ii) unclear. In any event, the Productivity Commission’s rejection of ISDS developed from the following premises:[70]

1. Bilateral trade and investment initiatives should not take precedence over multilateral and unilateral arrangements;

2. Foreign investors should not be provided greater rights over local investors;

3. Australia should not be exposed to regulatory chill;

4. There is no clear evidence that ISDS significantly increases inbound FDI or otherwise benefits Australia;[71]

5. There is no overall benefit to utilising ISDS; specifically, Australia’s outbound investors do not and need not rely on the protections offered by ISDS as alternatives such as insurance and access to local courts provide ample protection; and

6. There are inherent problems associated with the ISDS system, such as the large size and costs of investor claims, the latitude and inconsistency of investment tribunal determinations, the lack of rigorous rules governing the conduct of arbitration, the absence of an appeals process, the threat of ‘institutional biases and conflicts of interest’, and a lack of transparency.[72]

The Gillard Government’s 2011 Trade Policy Statement literally followed all the recommendations of the Productivity Commission when announcing it would no longer seek to include ISDS provisions in any future treaties.[73] The Government’s principal concerns stated in that document were: (1) conferring greater rights to foreign investors; and (2) the onset of regulatory chill.[74] The Trade Policy Statement similarly established generalised ‘disciplines’ to guide the contours of Australia’s future trade policy, including a statement that bilateral and regional agreements must always give way to the multilateral regime.[75]

Before we address each of the Productivity Commission’s six premises listed above, it is useful to first turn to our general concerns as to the Commission’s methodology.

1 General Concerns with the Methodology

The Productivity Commission did not fully analyse or investigate any of the perceived criticisms. Instead, it relied on a few select reports and cases. Given the overall conclusion that ‘[e]xperience in other countries demonstrates that there are considerable policy and financial risks arising from ISDS provisions’, the lack of breadth, depth and rigor in analysis is striking.[76] While the Productivity Commission acknowledged that some of the problems associated with ISDS can be ameliorated through the design of the relevant provisions, it nevertheless concluded that significant risks would remain — again without sufficient analysis or identifying exactly what risks, in its opinion, would remain.[77] If it had, of course, there would at least have been a benchmark on which further analysis could have been undertaken.

Curiously, while the Productivity Commission reports provide detailed analysis of traditional trade issues, the examination of investment issues and barriers is much more simplistic, shallow and cursory. Given the Government’s reliance on the 2010 Productivity Commission Report for a wholesale shift in policy, the brevity and selectiveness of the 2010 Report is rather surprising.

While it is unnecessary to review all of the Productivity Commission’s methodological faults, it is useful to provide a few examples.

(a) Conflation of Trade and Investment Issues

Simply stated, the Productivity Commission does not seem to have a reasonable understanding of the field of investment as distinct from trade. Indeed, the Commission’s asymmetrical focus on trade ramifications appears to have conflated the effects of regulatory barriers on investment and trade. For example, where the Commission selectively focuses on the liberalisation of border restrictions on capital (ie screening processes), it concludes that the direct economic impact of Australian investment and services provisions in FTAs ‘to date have been modest’.[78] The cross-contaminating of results between investment and trade is problematic. Unlike in trade (and particularly trade in goods), the critical barriers of FDI are not as readily quantifiable as they seldom take the form of border measures (such as tariffs). Most investment restrictions take the form of behind-the-border regulatory interventions (such as discriminatory or arbitrary regulatory process). Yet, the Productivity Commission is rather disengaged with assessing the likelihood and economic impact of these behind-the-border barriers.

(b) Lack of Analytical Depth

Another serious concern is the Productivity Commission’s failure to engage in any meaningful analysis of the investment jurisprudence or of Australia’s treaty practice. Instead, the Commission mostly applied generic data to Australia’s situation. One such example is the superficial reliance on data published by the United Nations Conference on Trade and Development (‘UNCTAD’), which provides little indication of Australia’s investment dynamic within the Asia-Pacific region.[79] Worse still, instead of engaging with or even citing case law, the Commission report relied on the selective citations from a single secondary source, which is again UNCTAD.[80] Such basic errors in research raise serious doubts about the quality of the report and the extent to which it was relied on to influence and shape policy.

(c) Failure Adequately to Engage with the Benefits of ISDS

While the Commission readily accepts the criticisms of ISDS, it appears almost hostile to the benefits of ISDS. For example, it is often stated in the literature that ISDS is an accepted and preferred method to combat blatantly protectionist or discriminatory acts by host States.[81] However, the Commission dismisses this claim almost out of hand. With only a cursory review of a few studies, the Commission concluded that there is ‘evidence that, in practice, host governments are not systematically biased against foreign investors’.[82] Kurtz and Nottage question the rigour of the Commission in this regard by stating: ‘In effect, the Commission, by relying on a handful of studies, has concluded that there is no risk of protectionism whatsoever at play in the formation of host State policy towards foreign investment.’[83]

The Commission’s position is an obvious overstatement and, more fundamentally, a sweepingly broad statement to make on the basis of incomplete and selective research.

(d) Failure to Consider the Circumstances of Current and Potential Treaty Counterparties

Yet another concern is that the Productivity Commission did not consider whether the decision to include or exclude ISDS should be based on the particular treaty partner’s circumstances, including forecasted investment flow or domestic legal protections available to investors. Such a comparative analysis could constitute a basis adequately to assess the utility of ISDS, particularly in the case where, as stated above, there does not appear to be any correlation between some of these circumstances and Australia’s practice of including or excluding ISDS.

Generally, the 2010 Productivity Commission Report and the 2015 Productivity Commission Review fail to engage with the basis or reasoning to justify Australia’s use of ISDS in past treaties. The Trade Policy Statement appears to have disregarded pertinent information such as inward and outward trends and expected forecasts into the future. In this regard, it is not only a matter of attempting to provide protections for outbound Australian investors, but also recognising that throughout Asia and other parts of the world traditional recipient states of investment are increasingly becoming outward investors and, as such, those states are likely to be seeking assurance for their investors. Again, one would expect that the Australian Government would have considered such trends, and attempted to determine the impact and implications of its policy shift on the direction of inbound FDI. This is particularly important as Australia is becoming increasingly dependent and economically tied to Asia, a region where almost all nations are accelerating the adoption of ISDS.

2 Australia’s Reasons for Rejecting ISDS

This section provides a deeper analysis of the basis relied on by the Productivity Commission and Australian Government for rejecting ISDS.

(a) Multilateralism and Unilateralism over Regionalism and Bilateralism

The Trade Policy Statement stated that ‘[m]ultilateral agreements offer the largest benefits ... [while] [r]egional and bilateral agreements must not weaken the multilateral system — they must be genuinely liberalising, eliminating or substantially reducing barriers to trade’.[84] Similarly, the Trade Policy Statement supported unilateral (domestic) reform for the purpose of attracting foreign investment.[85] Both the Productivity Commission and Trade Policy Statement advised against using the ‘bargaining chip’ approach to seeking investor protections from counterparties,[86] with the Government even eloquently stating: ‘Using domestic reform as a bargaining chip in negotiations is akin to an athlete refusing to get fit for an event unless and until other competitors also agree to get fit.’[87]

In eschewing bilateralism and regionalism in favour of multilateralism, the Australian Government failed to appreciate the practical realities of establishing a global agreement.[88] The international investment regime has naturally and gradually evolved through a network of BITs and regional agreements and previous attempts to codify these efforts into a multilateral treaty have failed. Most recently, the Organisation for Economic Co-operation and Development (‘OECD’) failed in the 1990s in an attempt to negotiate a multilateral agreement on investment due to disagreements on particular substantive and procedural standards.[89] Perhaps at that time such a multilateral regime was premature and the attempt over-ambitious.[90] But even today, as traditional FDI importers become exporters, it would be difficult to achieve consensus on a multilateral treaty model. Differences in standards, both substantive and procedural, are common among domestic regimes and an attempt to establish a global standard may not be desirable. Thus, bilateral and regional agreements offer a more practical link to multilateralism allowing for a dynamic and naturally evolving process, rather than being forced by a top-down approach.

Another relevant consideration omitted from the Australian Government’s analysis is the ability of investment treaties to allow states to ‘tap into’ a treaty network that provides better substantive standards of protection through the ‘most favoured nation’ (‘MFN’) clause.[91] For example, as a result of Australia securing an MFN investment guarantee in the ChAFTA, it may now ‘capitalise’ on any better terms China subsequently offers to third party investors.[92] These benefits are automatic, without the need to incur transaction costs in renegotiating the original treaty. The use of an MFN clause in the ChAFTA could be especially beneficial in light of the strong network of economies that China is currently negotiating agreements with, namely the US and the EU. Given the negotiating power of these two economies, it is likely that these agreements will contain more substantial investment protections than those contained in the ChAFTA. Where ISDS does not exist in treaties, Australian investors will not be able to make use of MFN and other clauses adequately to protect and enforce their rights.

Until a multilateral system eventuates, there are two other tangible benefits for Australia to continue engaging with the bilateral and regional process. First, Australia can use competing templates of investment agreements to develop best practices (of legal norms and procedural rules) to advance the specific needs and priorities of Australia. Second, Australia is better positioned to shape the ISDS mechanism according to its concerns as a crafter, drafter and mere participant as the system evolves, rather than after having entirely exited that system.

(b) Conferring Greater Rights on Foreign Investors

That foreign investors have greater rights than any other local investor is one of the major premises of the Australian Government’s approach for rejecting ISDS.[93] But in adopting this approach, it reinterpreted (or misinterpreted) the national treatment principle to argue against ISDS, with the Trade Policy Statement stating:

The Gillard Government supports the principle of national treatment — that foreign and domestic businesses are treated equally under the law. However, the Government does not support provisions that would confer greater legal rights on foreign businesses than those available to domestic businesses.[94]

The national treatment principle is a norm permeating the acquis of both investment[95] and trade law,[96] and providing for equal competitive opportunity between foreign and domestic firms. In the investment context, it means that a foreign investor should not be treated less favourably as compared to the local investor.[97] Given that such substantive rights take a different form to the laws of the host State, the national treatment principle is designed as a common benchmark to facilitate equality between foreign and local investors.

Curiously, the Trade Policy Statement and Productivity Commission reports claim that ISDS effectively requires the host State to provide the foreign investor positive discrimination in their favour, and receive substantive rights over-and-above that of a domestic investor.[98] Consequently, the Productivity Commission (relying solely on one academic submission) concluded that ISDS can thereby disadvantage the opportunities of domestic investors, as compared to those of foreign investors.[99] As such, the Productivity Commission quoted the submission of Aisbett and Bonnitcha stating that ‘productivity may fall as a result of the investment agreement as efficient domestic producers are displaced by less efficient but better politically-insured foreign firms’.[100]

The weight of evidence (including by Nobel Laureate Joseph Stiglitz)[101], however, sees the guarantee of national treatment as a tool to improve competition in the host State market by allowing the most efficient and innovative investor to operate in the host State’s market. The Australian position is therefore based on a flawed premise: such obligations are equally designed to remove any discrimination against the foreign investor, not as a guarantee to discriminate in favour of that investor.

(c) The Hypothesis of Regulatory Chill

Both reports of the Productivity Commission and the Trade Policy Statement claim that ISDS places undue restrictions on governments regulating in the public interest.[102] This claim was principally based on Australia’s exposure to potential ISDS claims,[103] especially the then pending Philip Morris case (challenging legislation on plain packaging of tobacco products), and particularly on Australia’s mounting costs to defend that claim.[104]

Australia’s investment policy should not be disproportionately based on how many claims it has or may face and, similarly, how many claims Australian investors have or will make. At best, whether Australia faces claims or Australian investors use the system to litigate against other states should be considered equally with other guiding criteria. That being the case, as to the Productivity Commission’s apprehension regarding potential exposure to ISDS cases, it is interesting to note that ‘[o]ver 90 percent of the nearly 2,400 BITs in force have operated without a single investor claim of a treaty breach’ and that while ‘[t]he number of disputes filed in the past 10 years has increased’, the increase ‘has been proportional to the rise in outward foreign capital stock’.[105] The Philip Morris claim was the first known claim against Australia, while Australian investors have enforced their rights using ISDS in at least four cases.[106]

The Productivity Commission inference that investment agreements can lead to regulatory chill is likewise not based in evidence. On the contrary, the Commission made no attempt to provide any supporting studies or evidentiary basis to determine whether the concern is more apparent than real. Had the Commission researched the literature, it would have found that studies canvassing a broad range of cases have not found any evidence of regulatory chill.[107]

More controversially, an argument could even be made that ‘regulatory chill’ is not to be feared and that some ‘chill’ could even be prudent for Australia’s regulatory framework, and thus a benefit to all Australian nationals.[108] Australia benefits from its embrace of international investment standards such as fairness and a reasonable expectation of a predictable investment environment in that these standards prevent sudden reversals of (politically-based) policies that expose all investors to harm.[109] Accordingly, in certain circumstances, international legal protections may be seen to reinforce democratic values of investors (local and foreign) and the general public, rather than undermine them.

Indeed, even if the prospect of regulatory chill is potentially real, our underlying concern and criticism of the Australian Government remains — its position was not premised on a thorough assessment of the relevant literature or contextualised in any way.

(d) The Finding that ISDS Does Not Attract FDI

The 2010 Productivity Commission Report stated that ‘committing to ISDS provisions does not influence foreign investment flows into a country’[110] and maintained this position in the 2015 report.[111] Such a position is problematic for a host of reasons. It is true that recent econometric studies as to a causal relationship between investment treaties and an increase in inbound foreign investment have yielded conflicting results.[112] However, we have noted above the difficulty is isolating the effects of investment agreements and ISDS on FDI flows from other potential economic factors. There is also a real risk that as additional investment agreements are entered into and standards continue to rise that trade and investment may be incrementally diverted away from countries which lack the full suite of expected protections.[113]

Notwithstanding these issues, the main issue with the Productivity Commission reports is again that instead of fully engaging with this complex literature, the Commission rather surprisingly considered only one study (that was in itself more than 10 years old and inconclusive) for its sweeping conclusion that ISDS does not lead to increased foreign investment.[114] As such, while the econometric evidence relating to FDI flows and investment agreements with ISDS remains mixed and based on aggregate worldwide FDI, the Productivity Commission ought to have identified these shortcomings and thus qualified the conclusion of the reports on this basis.[115]

To be fair, the 2015 Productivity Commission Review does begin to address the empirical data on the destination of inbound and outbound FDI.[116] Somewhat strangely, however, the Commission concluded that since FDI flows in the largest quantities to developed states that have ISDS provisions, ISDS provisions are not necessary in order to foster further flows. In similar circular reasoning, the Commission essentially concluded in regards to outbound FDI to less-developed countries that since these countries represent a small proportion of Australia’s total outbound FDI, ISDS does not appear materially to contribute to outward investment.[117] Interestingly, the Commission reported but failed to engage with the statistics showing that despite the small proportion of outbound FDI with treaty partners adopting ISDS, the percentage has doubled over the past 10 years — perhaps as a result of the large number of investment agreements negotiated since the 1990s.[118]

There are additional errors with the Productivity Commission’s 2015 analysis. First, its analysis is limited to a sample of two states (Singapore and Hong Kong), on the basis that those are in the ‘top ten source and destination’ jurisdictions.[119] Second, the timeframe chosen (namely, 2003–13) is somewhat arbitrary. For example, the Australia–Hong Kong BIT entered into force in 1993 and it is likely that any influence to FDI that ISDS would have been concentrated throughout the 1990s.[120] The Productivity Commission makes the same error in measuring FDI for a series of aggregated ‘Other ISDS’ states where again most of those investment treaties date from the 1990s.[121]

Second, the Productivity Commission fails to appreciate that the success or failure of ISDS need not be solely measured by FDI statistics. One example of unmeasurable benefits is the ability to provide investors with a reasonable degree of comfort (of stability and predictability), which can influence the decision to invest in a particular jurisdiction. Another related example is the promotion of the tighter integration of industrial supply chains throughout North America as a result of the NAFTA.[122]

The Productivity Commission’s failure to appreciate important, but less obvious, factors is not only reflected in the Commission’s analysis of FDI statistics, but also in its subsequent conclusion that, on the basis that only three Australian investors have commenced ISDS proceedings, there is an ‘apparent lack of evidence regarding the effects’ of ISDS.[123] A representation of three investors initiating legal action does not necessarily indicate that other investors are not relying on ISDS provisions to guide their decision to invest and/or not utilising this enforcement mechanism in negotiations with the host State.

The 2015 Productivity Commission Review concluded that a detailed impact assessment that quantifies the national economic impact and distributional effects, as well as the costs and benefits of, inter alia, ISDS ought to be ‘comprehensively analyse[d] ... well before’ signing a particular investment agreement.[124] While it is certainly prudent for a nation to carry out feasibility studies before entering into an agreement, the Productivity Commission has set an unreasonable, and even impossibly high, standard. Andrew Stoler, a dissenting member of the 2010 Productivity Commission Report bluntly states that if governments ‘don’t have the tools to make those kind of measurements, it’s not exactly fair game to insist that you have to make those measurements before you decide whether the agreement is a good one or not’.[125]

(e) Cursory Treatment of the Benefits of ISDS

The Productivity Commission determined, both in 2010 and 2015, that since there were no apparent market failures requiring rectification, there was no overall benefit of utilising ISDS.[126] Yet, the Commission’s analysis of the potential benefits arising from ISDS was less detailed when compared to the analysis of the costs of implementing ISDS (even though incomplete and including several disconcerting assumptions). The Commission did not mention any literature or provide real world examples of ISDS being used directly or even indirectly to enforce treaty protections, nor did it concede that ISDS may, in some instances, provide more complete investor protection than the alternatives it sets out. This is unfortunate and, again, gives the impression that the 2010 and 2015 reports not only lack rigour, but are inherently biased.

(i) The Absence of ‘Systemic Bias’ against Foreign Investors

At its core, the analysis and conclusions of the 2010 and 2015 reports of the Productivity Commission on the utility and purpose of ISDS result from an erroneous assumption: that foreign investors do not ‘face systematic biases against them’ compared to local investors.[127] The assumption was based not on a study of the rich literature on this point, but on two studies (both based on the same survey) published in the mid-2000s.[128] Of greater significance is the fact that these studies solely focus on the Southeast Asia region and are, thus, of limited relevance to Australian investment flows. Further, these findings contradict various recent studies that more concretely demonstrate the concerns of foreign investors operating in such countries as China,[129] Vietnam[130] and Indonesia.[131] In short, reports of unfair and discriminatory treatment against foreign investors is not only well-known, but also commonplace.

Consequently, the statement that there is ‘evidence that, in practice, host governments are not systematically biased against foreign investors’[132] is not only sweepingly broad, but does not logically support the Productivity Commission’s conclusion that ISDS does not offer foreign investors any comfort or protection against discriminatory or unfair interventions. Instead, the Commission largely reduced its analysis to the question of whether there was any measurable economic market failure that could be overcome by ISDS.

(ii) The Lack of Industry Feedback

Again rather peculiarly, the 2010 Productivity Commission Report justified its position by stating that it received no feedback from Australian businesses or industry associations as to the value of ISDS protections.[133] While the lack of input was indeed an oversight by the business and legal community, it may be too far a step to conclude that a lack of submissions to a broad enquiry on trade and investment agreements indicates a lack of interest in or support of ISDS. Indeed, the more likely inference is that stakeholders were not attuned to the Commission’s project as the vast majority of the 2010 report focused on trade rather than investment and that smaller investors may have less knowledge of the benefits of ISDS and fewer resources to dedicate to making submissions to government committees. Indeed, the Commission’s conclusion is even inconsistent with the Trade Policy Statement’s claim that ‘[i]n the past, Australian governments have sought the inclusion of [ISDS] in trade agreements with developing countries at the behest of Australian business.’[134]

More importantly, in making its conclusion the Commission unduly dismissed the factual record that demonstrates the value of ISDS to Australian industries. Indeed, Australian foreign investors have availed themselves of the benefits of ISDS in claims against India, Indonesia and Pakistan.[135] Other investors have, no doubt, used the presence of ISDS in an investment treaty to successfully resolve disputes before they reach binding arbitration.

(iii) The Asymmetrical Cost-Benefit Analysis

Underlying the Productivity Commission’s flawed analysis is an asymmetrical costbenefit calculation. For example, the costs incurred (by the Australian Government) are not counterbalanced by both: (i) the benefits from inbound investors into Australia; and (ii) the benefits to Australia’s outbound capital.[136] Unlike foreign traders, investors are exposed to the inherent immobility of FDI, with long-term projects, and high up-front (sunk) capital costs, with minimal or no alternative use value. Such limiting factors were not considered by the Australian Government or the Productivity Commission. The Australian Government simply minimised and dismissed Australian investor risks,[137] and, in so doing, effectively placed a burden on Australian investors to take into account the associated economic, political and legal risks, while removing its responsibility to protect its investors.

In addition, the Productivity Commission, and subsequently the Australian Government, failed to recognise or engage with the possibility that a withdrawal from ISDS may tempt foreign investors to relocate productive operations (that are beneficial to Australian industries and consumers) away from Australia in order to obtain enhanced treaty benefits elsewhere (through legitimate investment agreement planning). Similarly, the Productivity Commission and Government also failed to address whether the withdrawal from ISDS might incentivise savvy Australian investors to structure investments through intermediary countries with existing investment treaties containing ISDS provisions rather than risk being deemed an ‘Australian investor’ and losing the opportunity to fully enforce treaty rights.

(iv) Exaggerated Benefits of Substitutes of ISDS

The Commission inadequately identified and evaluated alternative strategies to protect Australian foreign investors. The suggested alternatives for foreign investors — namely recourse to domestic courts, obtaining political risk insurance and using investment contracts to mitigate risk— are problematic in both their methodology and outcome. Each is briefly addressed in turn.

Court Processes

Past statements of the Australian Government and the two Productivity Commission reports did not fully analyse whether domestic courts provide effective recourse for Australian foreign investors, as well as whether there is a net benefit in permitting investors to choose between initiating domestic court actions as an alternative to ISDS. Rather, the Productivity Commission conceived that the most practical option was to resort to domestic courts. Logically, the fact that the Trade Policy Statement and Productivity Commission make a case against utilising ISDS does not, in itself, infer that domestic courts should be preferred. Simply stated, the Australian Government failed to consider the ramifications for Australian foreign investors of relying on domestic courts. Table 1 (below) provides a brief comparison of the benefits and criticisms of arbitration as compared to domestic courts.

Table 1: General benefits and criticisms of ISDS arbitration, compared to domestic

court process[138]

|

Benefits of Domestic Court Actions

|

Benefits of ISDS Arbitration

|

|

Domestic courts are bound by established forum procedures and predictable

rules of evidence.

|

Flexible process.

|

|

Courts usually have safeguards to correct errors in law and any curtailment

of procedural rights, through appeal procedures.

|

Ability to apply to domestic court (for non-ICSID

cases)[139] to have an award set

aside for procedural safeguards (departure of established process and failure to

provide adequate reasons for

award). Annulment proceedings are an extraordinary

process and more limited in scope than appeal to a domestic court.

|

|

Inconsistency of international arbitration awards. National law ought to

govern the rights of foreign investors.

|

Relative to the various laws of various host states, the applicable law

(the terms of the investment agreement) in ISDS is uniform

and

predictable.

|

|

Domestic courts ought to decide cases involving foreign investors according

to domestic law, and incorporate international investment

laws into that

domestic law. It is a traditional characteristic of sovereignty.

|

Allowing domestic courts to determine investment disputes according to

domestic law, and incorporating international investment laws

into that domestic

law, would result in inconsistent determinations between states and would likely

be subject to determinations

that provide greater deference to the host

State.

|

|

Domestic laws are considered, including public interest concerns, and are

more likely to be applied consistently. Arguably, host States

are more likely

than ISDS tribunals to apply a public interest defence with greater deference to

the host State.

|

Domestic laws are not irrelevant and are considered, depending on the

nature of the claim (eg an umbrella clause) or the express provision

of the

investment agreement (referring to domestic law).

|

|

A domestic court of the State that is party to an investment treaty is the

appropriate forum to resolve an investment dispute.

|

Where the actions or omissions of the domestic court of the State that is

party to an investment treaty is the subject of a dispute,

that domestic court

is not the appropriate forum to resolve an investment dispute.

|

Investment Contracts and Political Risk Insurance

Resort by the Productivity Commission and the Australian Government to investment contracts (with dispute resolution clauses) may sound like a simple and attractive alternative, but, in practice, may not be viable.[140] First, such a contract would likely be subject to the law of the host State (despite attempts to ‘contract out’)[141] and, in the absence of an agreement with ISDS, investors would remain vulnerable to arbitrary or discriminatory application of the law.

Second, the Productivity Commission’s analysis of political risk insurance is incomplete. The 2010 Productivity Commission Report solely focused on the availability of political risks insurance against expropriation, but failed to look at the practical reality.[142] In practice, such coverage is often short-term, limited and only available up to a certain monetary amount. Importantly, political risk insurance against expropriation does not typically cover other forms of illegitimate government interference commonly protected by other international investment norms, such as ‘fair and equitable treatment’. In recent years, investors have relied on the ‘fair and equitable treatment’ obligation more frequently and successfully than other breaches, such as expropriation.[143] Similarly, political risk insurance policies[144] may be easier and more cost effective to procure where there is an investment agreement between the investor’s home State and the host State. In this regard, Gordon states: ‘Risk assessments under many [political risk insurance] programs often look at the existence of BITs or other agreements’.[145] As such, political risk insurance is unlikely to be an adequate substitute for a treaty containing ISDS.[146] Dissenting Commissioner Stoler bluntly stated that the argument for the possibility to obtain political risk insurance as a substitute for treaty-based investor protections ‘is analogous to arguing against the need for a fire department because homeowners can buy property insurance’.[147]

Overall, while the Productivity Commission provided some sensible strategies analysing the value of the investment treaty regime (such as the impact assessment prescribed in the 2015 review),[148] the Commission overestimated the risks of ISDS, while significantly underestimating both its general and specific benefits. The Commission also too casually posed alternatives to ISDS that, in practice, pale in comparison to ISDS and fall well short of providing security and predictability to investors.[149]

In the absence of a transparent investment policy, we can only surmise whether and, if so, to what extent the temporary mining boom, the Philip Morris claim against Australia, serious institutional concerns about ISDS or a general apprehension with bilateral and regional trade arrangements played a role in the Australian Government’s 2011 Trade Policy Statement. What is clear, however, is that the Government failed to isolate these concerns from one another and, as a result, failed to engage in a meaningful debate regarding the merits of ISDS.

A broad policy statement that is fundamentally based on protecting sovereign interests and ignores the merits of ISDS can have various practical flow-on effects. These effects differ in scope, ranging from impacts on the development of Australia’s industries, to Australia’s position in the global political economy and the broader international investment regime. This section also makes the case that, like any other comparative advantage, Australia ought to utilise its respected, first-rate domestic legal system to obtain reciprocal benefits throughout bilateral agreements. Yet, we propose that this should only be utilised once some threshold criteria (such as current and anticipated FDI flows with the counterparty, its GDP and/or the status of its legal system) have been met.

Given Australia’s position in the global political economy, an outright blanket rejection of ISDS founded on inadequate discourse, incomplete analysis and specious methodology could have unintended consequences. One such potential consequence, or ripple effect, will be Australia’s loss of influence in improving the functioning of the integrated investment treaty system. Removing itself outright from the pervasive international system will deny Australia the opportunity to revise or improve the legal norms. For a country of its size, Australia has had considerable influence in the direction of certain treaty language, in particular for ensuring treaties contain safeguards for non-discriminatory public welfare measures taken by the State.[150] Withdrawing from the regime would mean Australia would no longer be able to craft and shape treaty language — in the process, of course, Australia’s influence in this domain would wane considerably.

Similarly, removing itself from the regime may affect Australia’s competitiveness as future investment agreements increase standards and potentially make signatory counties more attractive investment destinations. This is particularly important at the present time when large regional treaties are being negotiated and as China’s ‘Belt and Road’ Initiative searches for large-scale investment initiatives.[151] Australia, with its investors, is a player in these developments, and it would seem prudent to be a crafter and drafter of investment norms, rather than enter the stage late without any power to influence the development of the norms.

Australia’s position in the Trade Policy Statement is clear — ISDS should not be used as a bargaining chip to obtain favourable concessions — and appears to be based on the notion of protecting sovereignty. However, again, it ignores the reality of the dynamics of the negotiation process. Trade and investment negotiations, or in fact any international negotiation, involve a reduction of sovereignty in some sense as the parties agree to an obligation ostensibly in return for an overall benefit. In the context of the investment legal regime, states agree to limit their discretion in the treatment of foreign investors, in consideration for certain benefits and concessions and (in no small part) to attract capital. A blanket refusal to use the ‘ISDS card’ not only removes a large degree of flexibility from the negotiators, but also denies Australia’s ability to use its comparative advantage as leverage throughout the negotiations, which, in this case, is a more advanced domestic legal system. That is, if Australia has the benefit of an advanced domestic court system, surely it should realise that advantage throughout treaty negotiations, just as it would for any other of its industrial advantages (such as beef and agricultural production). This is not even a theoretical point, with evidence that Australia did just this in the TPP negotiations by using its anti-ISDS reservation as a bargaining chip against the US’s desire to extend the length of test data protection for biologic pharmaceuticals.[152] Taking away this potential to bargain and achieve a more tailored and potentially more appropriate agreement seems not to be in Australia’s interests.

To date, the Australian Government’s position and debate has revolved around the specifics of ISDS and avoiding the most important issue: the lack of applicable guidelines in Australia to form the basis of a prudent treaty strategy. ISDS and other concessions are only one component of the larger agreement, but, in reality, any provision (including ISDS) should only be entered into where there is a net perceived long-term benefit to Australian industries and investors, consumers, and the overall national economy.[153] While ISDS appears to facilitate these goals by providing the right to enforce the underlying treaty obligations, Australia should have criteria that it applies before considering whether to place ISDS (or any concession or issue) on the negotiating table.

This Part explores whether a principled, but flexible, investment and ISDS policy can be formulated with specific regard to Australia’s interests and taking account of the regional and global political economy. It will specifically address whether the concerns of the Productivity Commission and the ‘case-by-case’ approach as applied by the current Government can be reconciled.

We propose two components to a consistent ISDS policy: (1) a principled threshold to determine when ISDS will be on the negotiating table (such as net FDI flows and legal protections and enforcement mechanisms available for outbound investors); and (2) a template or model BIT (with ISDS provisions and substantive investment obligations) that should be considered throughout the treaty negotiations if the ISDS threshold is met. Before advancing this proposal, we address the content of the model BIT, and suggest provisions that respond to the abovementioned concerns of the Productivity Commission.

Australia would be prudent to consider adopting reform measures that have recently been included in investment treaties and model BITs elsewhere. Again, it is more than a little curious that the 2010 and 2015 Productivity Commission reports failed to consider the new models of investment protections, but based their analysis on outdated practices from antiquated treaties. By ignoring recent treaties, the Commission failed to cover the substantial reforms and departures from investment treaty practice of the 1980s–2000s. Some of the more important trends in treaty drafting, which we refer to as ‘ISDS+’, are outlined below.

1 Protection to Regulate for Public Interest

ISDS provisions can be drafted to address apparent concerns of ‘regulatory chill’, and there is of course no magic formula in doing so. Such concerns can be addressed in a variety of ways. The treaty can expressly provide for the protection of the State’s legitimate public interests, such as public health and morals, culture, natural resources and the environment. One example of what has become a common provision in relation to expropriation, comes from the AUSFTA and reads:

Except in rare circumstances, nondiscriminatory regulatory actions by a Party that are designed and applied to achieve legitimate public welfare objectives, such as the protection of public health, safety, and the environment, do not constitute indirect expropriations.[154]

In conjunction with a narrowing of obligations as seen above, treaties can include a general exception clause that further protects measures ‘necessary’ to safeguard public interests such as health, environment, morals and culture. Such clauses are modelled after the general exceptions of the World Trade Organisation’s (‘WTO’) General Agreement on Tariffs and Trade (‘GATT’) (art XX)[155] or General Agreement on Trade in Services (‘GATS’) (art XIV)[156] and generally provide:

Provided that such measures are not applied in an arbitrary or unjustifiable manner, or do not constitute a disguised restriction on international trade or investment, nothing in this Agreement shall be construed to prevent a Contracting Party from adopting or maintaining measures, including environmental measures: (a) necessary to ensure compliance with laws and regulations that are not inconsistent with the provisions of this Agreement; (b) necessary to protect human, animal or plant life or health; or (c) relating to the conservation of living or non-living exhaustible natural resources if such measures are made effective in conjunction with restrictions on domestic production or consumption.[157]

States have also created other public policy regulatory space along various planes, including vertical arrangements such as industry-sector carve-outs (ie natural resources, tobacco, mining industry, etc)[158] or for various types of measures, such as taxation.[159] Another possibility is to utilise a hybrid approach that provides carve-outs pertaining to a particular substantive obligation, such as national treatment or MFN.

Such exceptions could also utilise and adopt the ‘legitimate regulatory distinction’ test[160] applied in the WTO under art 2.1 of the Technical Barriers to Trade Agreement.[161] Under this analysis, a violation of, say, the national treatment obligation is permitted so long as the respondent State can demonstrate that there is a rational nexus between the detrimental treatment and the policy objective of the measure. A similar approach has been applied in the investment context in Pope & Talbot v Canada and Feldman v Mexico[162] and Bilcon v Canada tribunals.[163]

The recently negotiated TPP, even if it will not come into force, remains indicative of drafting trends. In this regard, the TPP is perhaps the gold standard (from the perspective of the degree of state sovereignty retained) for its attempt to exempt ‘public interest’ regulation and ‘to protect legitimate government regulation in the areas of health and the environment’.[164] For example, the TPP contains a novel, if controversial, type of the vertical carve-out whereby states defending an ISDS claim brought by a tobacco company can unilaterally preclude such a claim by invoking the ‘denial of benefits’ clause. While such clauses appear to be more effective for states than the general policy exceptions, a blanket tobacco company preclusion is potentially problematic as it may itself lead to abuse and, given that the State can raise the defence after the filing of a claim, such clauses raise serious due process concerns.

Another innovation along these lines is included in the ChAFTA, which allows for a joint state interpretation of a public welfare regulatory measure. Under that process, once an allegation as to a public welfare regulation is raised, the respondent State may issue a ‘public welfare notice’ specifying why the measure falls within the exception (also drafted similar to the GATT art XX exceptions).[165] The proceedings are then suspended for the treaty parties (ie China and Australia) to determine whether the alleged measure falls with the exception.[166] Such a determination by the treaty parties is binding on the tribunal.[167]

The semantics of each individually crafted clause is beyond the scope of this article; the point here is simply that exceptions and limitations to obligations exist and are readily drafted into modern investment treaties. These provisions seek to safeguard the sovereign’s inherent regulatory powers (to regulate for health, safety, morals and general welfare) with the overall goal of encouraging investment. Throughout the treaty negotiation process, Australia may ‘ratchet’ up or down such regulatory protections as it sees fit and depending on the particular counterparty’s circumstances. A complementary reform option is to maintain a broader membership of potential tribunal panellists (perhaps through a prescribed list of candidates) with expertise in not only international investment and/or trade law, but also public health, environmental and human rights law.[168] Similarly, the appointed tribunal could be encouraged (or required) to rely on consultants with this expertise for assistance and guidance (depending on the nature of the dispute). In addition, it could be mandatory that those arbitrators nominated by the parties have demonstrated a minimum understanding and experience in applying the Vienna Convention on the Law of Treaties in a consistent manner.[169] Such proposals have yet to be developed throughout the international investment regime. In fact, even the EU’s recent Investment Court proposal contained in the CETA[170] falls short of this level of specificity, but does specify that the judges appointed have a requisite degree of competence, including ‘demonstrated expertise in public international law’.[171]

It would be prudent for the Australian Government to consider such options as further safeguards of legitimate and non-discriminatory public policy. They are current, relevant and advanced by some measure over the provisions existing in older investment treaties.

2 Preventing Abusive Practices

A general concern surrounding ISDS is that it exposes a State to ‘abusive’ foreign investors, who could commence premature and pernicious claims or create opportunistic claims through restructuring of multinational corporations and treaty shopping. Here again, the Productivity Commission and the Australian Government collectively failed adequately to consider that treaties may be drafted in such a manner to carefully circumscribe ISDS access through measures such as:[172]

• Prescribing the definition of ‘investor’ to restrict the range of investors who qualify for protection under the treaty;

• Conditioning the commencement of an ISDS claim on a requirement that the investor exhaust local remedies (ie domestic courts or administrative tribunals of the host State). This condition may prescribe time limits (time-caps) in order to prevent abusive delays by the host State;

• Including denial of benefits provisions (such as those in NAFTA and CAFTA)[173], or bolstering the existing traditional provisions (as has been done in the TPP-11);[174]

• Including a specific summary procedure for claims alleged to be manifestly without merit (such as those in the CETA and proposed by the EU in the TTIP);[175]

• Including provisions to allow states to bring counterclaims against the foreign investor that initiated the claim, before the same tribunal;[176]

• Including a prescribed cap on the scope of substantive protections (such as fair and equitable treatment or MFN treatment), where there are concerns that certain international standards risk exposing the state to a standard greater than the domestic law.[177]

3 General Procedural Controls

Similar controls can be made to address the concerns of excessive procedural rights granted to foreign investors, and to address transparency concerns by states and the general public, such as:

• Prescribing ISDS provisions that mandate a negotiation and conciliation process as a condition to commencing investor–State arbitration. These may prescribe time limits with the ability of the parties to certify, on consent, that mediation has failed (in order to avoid undue delays).[178]

• Providing robust protections that appropriately balance transparency of proceedings, and preserving confidential information of the disputing parties.[179]

• Streamlining procedures that customarily create procedural bottlenecks, such as establishing standing panels to promptly determine arbitrator challenges.[180] Similarly, standing panels could be established to consistently interpret the institutional rules (the ICSID Convention,[181] ICSID Arbitration Rules,[182] and UNCITRAL Arbitration Rules[183]) in order to address concerns as to their inconsistent application.

4 Review Procedures for Legal Interpretations

While the ICSID Convention[184] maintains safeguards for parties regarding the conduct of the arbitration,[185] no practice exists to review awards for legal errors. The incorporation of an appeals process in the ICSID Convention has been considered but abandoned not only during the initial negotiations, but also at several stages thereafter.[186] That said, recent concerns as to the consistency of legal interpretations, which were not anticipated in 1965 when the Convention was signed, have caused the international community to reconsider the feasibility of an appellate mechanism. This mechanism became a central issue in the EU preceding the signing of CETA and throughout the TTIP negotiations.[187]

An appellate mechanism may be prescribed either within the underlying bilateral or regional agreement or perhaps through an independent multilateral agreement (similar in application to the ICSID Convention). Some recent treaties do provide a mechanism for states to establish such a body, such as the CETA,[188]

US–Chile FTA (2003),[189] CAFTA–DR (2004),[190] and KAFTA,[191] as well as other US agreements,[192] though the parties have yet to constitute such a body.

While Australia’s ‘case-by-case’ treaty policy appears to be pragmatic and flexible, uncertainty remains as to Australia’s expectations throughout treaty negotiations. A predictable and objective approach promotes efficiency and manages expectations of the counterparty, as well as the concerns of the public and statutory bodies designed to review the effects of the agreements before their implementation (such as the Joint Standing Committee on Treaties).

1 Threshold Criteria