Commonwealth Consolidated Acts Commonwealth Consolidated Acts

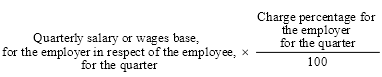

Commonwealth Consolidated Acts Commonwealth Consolidated Acts(1) An employer's individual superannuation guarantee shortfall for an employee for a quarter is the amount worked out using the formula:

where:

"charge percentage" , for an employer for a quarter, means:

(a) the number specified in subsection ( 2 ) for the quarter (u nless paragraph ( b) applies); or

(b) if the number specified in subsection ( 2) for the quarter is reduced in respect of the employee by either or both sections 22 and 23--the number as reduced.

"quarterly salary or wages base" , for an employer in respect of an employee, for a quarter means the sum of:

(a) the total salary or wages paid by the employer to the employee for the quarter; and

(b) any sacrificed salary or wages amounts of the employee for the quarter in respect of the employer.

(2) The charge percentage for a quarter in a year described in an item of the table is the number specified in column 2 of the item.

Charge percentage (unless reduced under section 2 2 or 23) | ||

Item | Column 1 | Column 2 |

1 | Year starting on 1 July 2013 | 9.25 |

2 | Year starting on 1 July 2014 | 9.5 |

3 | Year starting on 1 July 2015 | 9.5 |

4 | Year starting on 1 July 2016 | 9.5 |

5 | Year starting on 1 July 2017 | 9.5 |

6 | Year starting on 1 July 2018 | 9.5 |

7 | Year starting on 1 July 2019 | 9.5 |

8 | Year starting on 1 July 2020 | 9.5 |

9 | Year starting on 1 July 2021 | 10 |

10 | Year starting on 1 July 2022 | 10.5 |

11 | Year starting on 1 July 2023 | 11 |

12 | Year starting on 1 July 2024 | 11.5 |

13 | Year starting on or after 1 July 2025 | 12 |

(2A) If an employer makes one or more contributions (the no choice contributions ) to an RSA or a complying superannuation fund other than a defined benefit superannuation scheme, for the benefit of an employee during a quarter and the contributions are not made in compliance with the choice of fund requirements, the employer's individual superannuation guarantee shortfall for the employee for the quarter is increased by the amount worked out in accordance with the formula:

where:

"notional quarterly shortfall" is the amount that would have been worked out under subsection ( 1) if the no choice contributions had not been made.

Note 1: See also subsection ( 2E) and section 19A.

Note 2: Part 3A sets out the choice of fund requirements.

(2B) If:

(a) a reduction of the charge percentage for an employee for a quarter is made under subsection 2 2(2) in respect of a defined benefit superannuation scheme; and

(b) there is at least one relevant day in the quarter where, if contributions (the notional contributions ) had been made to the scheme by the employer for the benefit of the employee on the day, the notional contributions would have been made not in compliance with the choice of fund requirements; and

(c) section 2 0 (which deals with certain cases where defined benefit members cannot choose another fund) does not apply to the employer in respect of the employee in respect of the scheme for the quarter;

the employer's individual superannuation guarantee shortfall for the employee for the quarter is increased by the amount worked out in accordance with the formula:

where:

"notional quarterly shortfall" is the amount that would have been worked out under subsection ( 1) if no reduction were made under subsection 2 2(2) in respect of the scheme.

"number of breach of condition days" is the number of relevant days in the quarter on which, if a contribution had been made to the scheme by the employer for the benefit of the employee, those contributions would have been made not in compliance with the choice of fund requirements.

Note 1: See also subsection ( 2E) and section 19A.

Note 2: Part 3A sets out the choice of fund requirements.

(2C) The following days in a quarter are relevant days for the purposes of subsection ( 2B):

(a) if the value of B in the formula in subsection 2 2(2) for the quarter is 1--every day in the quarter; or

(b) in any other case--every day in the quarter that is in the shorter of the scheme membership period or the certificate period referred to in subsection 2 2(2).

(2CA) For the purposes of paragraph ( 2B)(b), if the employee is a defined benefit member of a superannuation fund, subsection 32C(2) applies in relation to the employee and the fund as if it did not include paragraph 32C(2)(c) (requirement that fund includes a MySuper product).

(2D) A reference in subsections ( 2A) and (2B) to an employer's individual superannuation guarantee shortfall being increased includes a reference to the shortfall being increased from nil.

(2E) The Commissioner may , after taking account, wherever appropriate, of the operation of section 19A, reduce (including to nil) the amount of an increase in an employer's individual superannuation guarantee shortfall for an employee for a quarter under subsection ( 2A) or (2B).

Note: The Commissioner must have regard to guidelines in force under subsection 2 1(1) when deciding whether or not to make a decision under this subsection.

(2F) If:

(a) subsection (2G) applies to one or more contributions for a quarter that were not able to be made by an employer to a particular fund for the benefit of an employee; and

(b) after the period of 28 days after the end of the quarter, the employer made those contributions to any fund for the benefit of the employee;

the Commissioner may reduce (including to nil) so much of the amount of the employer's individual superannuation guarantee shortfall for the employee for the quarter as is due to the lateness of those contributions.

Note: The Commissioner must have regard to guidelines in force under subsection 2 1(2) when deciding whether or not to make a decision under this subsection.

(2G) This subsection applies to a contribution for a quarter that was not able to be made by an employer to a particular fund for the benefit of an employee if:

(a) the employer attempts to make the contribution at a particular time; and

(b) at that time, there is no chosen fund for the employee; and

(c) at that time, the most recent notification to the employer:

(i) by the Commissioner; and

(ii) relating to a request by the employer (or by the employer's agent) for the Commissioner to identify any stapled fund for the employee;

is that the Commissioner is satisfied that the fund is the stapled fund for the employee; and

(d) the fund does not accept the contribution from the employer for the benefit of the employee.

(3) For the purposes of the definition of quarterly salary or wages base in subsection ( 1), disregard an amount in a quarter if:

(a) the amount would be covered by paragraph ( a) of that definition for the quarter (about amounts paid to the employee); but

(b) the amount is taken into account under paragraph ( b) of that definition (about sacrificed salary or wages amounts) for any quarter.

Note: This prevents double counting if a sacrificed salary or wages amount is later paid as salary or wages, instead of being contributed to superannuation.

(4) If the quarterly salary or wages base, for an employer in respect of an employee, for a quarter exceeds the maximum contribution base for the quarter, the employer's quarterly salary or wages base to be taken into account for the purposes of the application of subsection ( 1) in relation to the quarter is the amount equal to the maximum contribution base.