Commonwealth Consolidated Acts Commonwealth Consolidated Acts

Commonwealth Consolidated Acts Commonwealth Consolidated Acts(1) This section applies only in relation to RSAs and to superannuation funds other than defined benefit superannuation schemes.

Reduction of charge percentage where contributions are made by employer

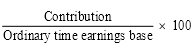

(2) If, in a quarter, an employer makes a contribution (other than a sacrificed contribution) for the benefit of an employee to a complying superannuation fund or an RSA, then the charge percentage for the employer (as specified in subsection 19(2)) for the employee for the quarter is reduced by the number worked out using the formula:

where:

"contribution" is the number of dollars in the amount of the contribution.

"ordinary time earnings base" is the number of dollars in the sum of:

(a) the ordinary time earnings of the employee for the quarter in respect of the employer; and

(b) any sacrificed ordinary time earnings amounts, of the employee for the quarter in respect of the employe r.

(3) A reduction under subsection ( 2) in respect of a contribution is in addition to:

(a) any other reduction under that subsection in respect of any other contribution; and

(b) any reduction under section 2 2.

Some contributions made after a quarter ends may be taken into account in the quarter

(6) A contribution to a complying superannuation fund or an RSA made by an employer for the benefit of an employee may be taken into account under this section as having been made in a quarter if it is in fact made within the period of 28 days after the end of the quarter.

(6A) A contribution (the actual contribution ) to a complying superannuation fund or an RSA made by an employer for the benefit of an employee may be taken into account under this section as having been made in a quarter if:

(a) the employer attempted to make a contribution to any complying superannuation fund for the benefit of the employee at a particular time within the period of 28 days after the end of the quarter; and

(b) at that time, the making of the attempted contribution was prevented by the operation of section 60F of the Superannuation Industry (Supervision) Act 1993 (consequences of 2 consecutive fail assessments); and

(c) the actual contribution is in fact made within the period of 56 days after the end of the quarter.

Certain contributions made before a quarter may be taken into account in the quarter

(7) A contribution to a complying superannuation fund or an RSA made by an employer for the benefit of an employee may be taken into account under this section as if it had been made during a particular quarter if the contribution is made not more than 12 months before the beginning of the quarter .

Sacrificed ordinary time earnings amounts taken into account in a quarter not to be taken into account for any other quarter

(7A) For the purposes of the definition of ordinary time earnings base in subsection ( 2), disregard an amount in a quarter if:

(a) the amount would be covered by paragraph ( a) of that definition for the quarter (about ordinary time earnings of the employee); but

(b) the amount is taken into account under paragraph ( b) of that definition (about sacrificed ordinary time earnings amounts) for any quarter.

Note: This prevents double counting if a sacrificed ordinary time earnings amount is later paid as ordinary time earnings, instead of being contributed to superannuation.

Contributions taken into account for a quarter not to be taken into account for any other quarter

(8) A contribution to a superannuation fund or an RSA made by an employer for the benefit of an employee that is taken into account under this section in relation to a quarter is not to be taken into account under this section in relation to any other quarter .

(8AA) A contribution:

(a) to a complying superannuation fund or an RSA made by an employer for the benefit of an employee after the end of a quarter; and

(b) in relation to which the employer's individual superannuation guarantee shortfall for the employee for the quarter is reduced under subsection 19(2F);

is not to be taken into account under this section in relation to any other quarter.

Contribution made when conversion notice has effect not to be taken into account under this section

(8A) A contribution to a superannuation fund or superannuation scheme made by an employer for the benefit of an employee at a time when a conversion notice has effect in relation to the fund or scheme is not at any time to be taken into account under this section.

Contributions to estate of deceased employee

(9A) If:

(a) an employee has died; and

(b) the employer would, if the employee had not died, have made a contribution to a complying superannuation fund or RSA for the benefit of the employee; and

(c) the employer pays to the legal personal representative of the employee an amount equal to the amount of the contribution that would have been paid;

the amount paid is taken for the purposes of this section to have been a contribution made by the employer to a complying superannuation fund or RSA for the benefit of the employee.

Charge percentage not to be less than 0

(10) The charge percentage for an employer for a quarter cannot be reduced below 0.

Reduction of notional earnings base if amount excluded from employee's salary or wages

(11) If an employee's notional earnings base includes an amount of the employee's salary or wages that, because of section 2 7 or 28, is not taken into account for the purpose of making a calculation under section 19, the employee's notional earnings base for the purposes of this section is taken to be reduced by that amount.

Reduction of ordinary time earnings base if amount excluded from employee's salary or wages

(12) If:

(a) because of section 2 7 or 28, an amount of an employee's salary or wages is not taken into account for the purpose of making a calculation under section 19; and

(b) a portion of that amount (which could be all of it) is included in the employee's ordinary time earnings base for the quarter in respect of the employer;

for the purposes of this section, the employee's ordinary time earnings base for the quarter in respect of the employer is taken to be reduced by an amount equal to that portion.

(13) Subject to subsection ( 15), if:

(a) an employer makes a deposit under the Small Superannuation Accounts Act 1995 in respect of an employee before 1 July 2006 ; and

(b) the deposit form that accompanied the deposit, in so far as the form relates to the deposit, did not contain a declaration that is false or misleading;

this section has effect as if the deposit were a contribution made by the employer for the benefit of the employee to a complying superannuation fund.

(14) Subsection ( 13) has effect despite section 9 of the Small Superannuation Accounts Act 1995 .

(15) If:

(a) an employer makes a deposit under the Small Superannuation Accounts Act 1995 in respect of an employee; and

(b) the employer receives a payment under Part 8 of that Act by way of a refund of the deposit;

this section has effect as if the deposit had never been made.

(16) In subsections ( 13) and (15):

"deposit" has the same meaning as in the Small Superannuation Accounts Act 1995 .

"deposit form" has the same meaning as in the Small Superannuation Accounts Act 1995 .